Stocks● Neutral

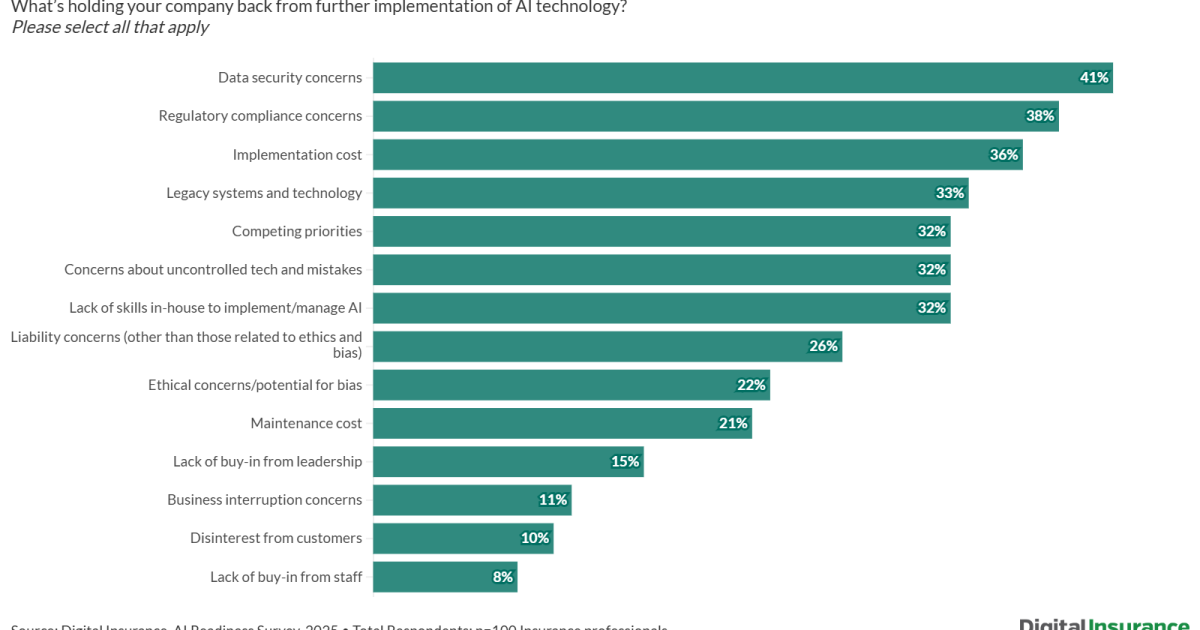

Cybersecurity Fears Stall AI Rollouts for 52% of Insurers

With 52% of insurance professionals fearing cyberattacks, carriers are prioritizing defensive infrastructure over AI, signaling a shift toward stability.

Continue with

The insurance industry is currently facing a significant friction point in its digital transformation roadmap as cybersecurity concerns begin to outweigh the perceived benefits of rapid AI deployment. According to recent data from Digital Insurance, 52% of insurance professionals now anticipate a near-term cyberattack, a sentiment that is directly influencing the pace and scope of their artificial intelligence initiatives. This shift in sentiment suggests that the industry is moving from an experimental phase into a more cautious, risk-averse posture regarding new technology infrastructure.

Security Constraints on Operational Scaling

The primary hurdle for carriers involves the integration of large language models and automated decision-making tools into sensitive data environments. Because AI systems require access to vast repositories of policyholder information and historical claims data, the potential for a breach creates a high-stakes barrier to entry. Carriers are finding that the cost of securing these AI pipelines often exceeds the immediate efficiency gains promised by the technology. This creates a bottleneck where the desire to modernize is being checked by the necessity of maintaining robust, air-gapped security protocols.

This trend is particularly visible in the following areas of insurance operations:

- The hardening of legacy data silos to prevent unauthorized AI-driven access points.

- Increased allocation of IT budgets toward defensive cybersecurity infrastructure rather than front-end AI development.

- A slowdown in the deployment of customer-facing AI agents due to fears regarding data leakage and regulatory non-compliance.