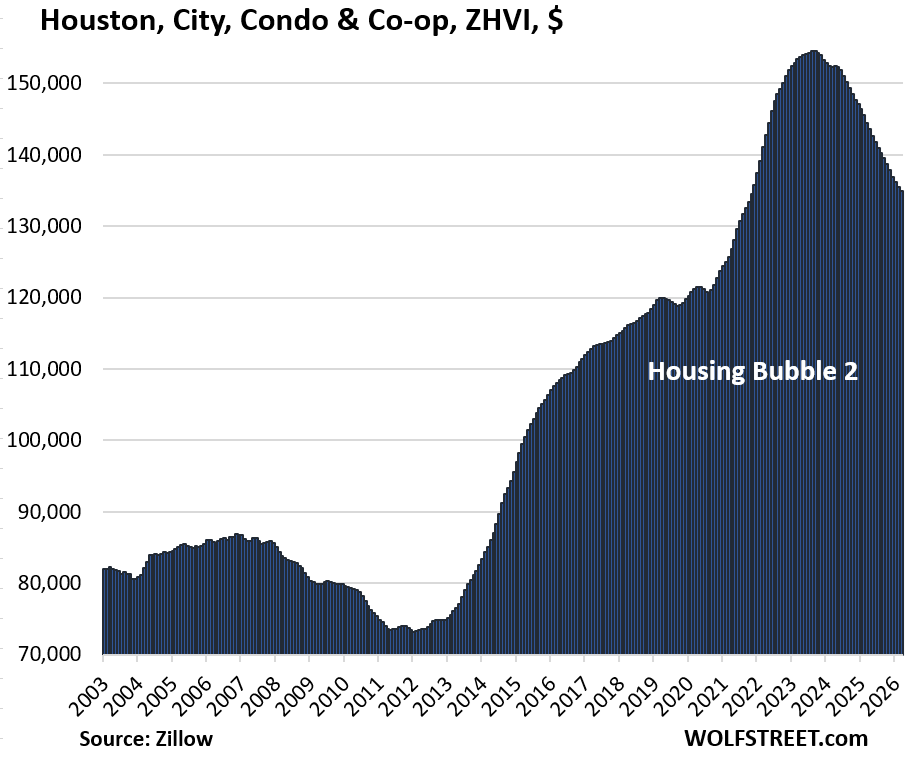

The residential real estate sector is currently navigating a sharp repricing event as condo valuations in 31 major markets have declined by 12% to 31%. This contraction reflects a structural shift in demand for high-density living, with some regions experiencing price levels that have retreated to valuations not seen in two decades. Oakland stands out as a primary example of this trend, recording a 31% decline that effectively resets the local market clock to early 2000s levels.

Regional Concentration of Asset Devaluation

The downward pressure on prices is not uniform but is heavily concentrated in specific urban centers that previously experienced rapid appreciation. St. Petersburg, Florida, has seen a 28% drop, while Austin, Texas, follows closely with a 26% decline. These figures suggest that the correction is most acute in markets where supply-side expansion outpaced local demand or where interest rate sensitivity has disproportionately impacted the mid-tier condo segment. The breadth of this decline across 31 distinct markets indicates that the issue is not isolated to a single geography but is instead a broader trend affecting the liquidity of multi-unit residential assets.

Structural Challenges for Mid-Tier Inventory

Condos face unique headwinds compared to single-family homes, particularly regarding homeowner association fees and the specific financing requirements for high-density residential properties. As borrowing costs remain elevated, the carrying costs for these units have become a significant deterrent for potential buyers. This environment forces a recalibration of price expectations, as sellers must compete with a larger pool of inventory that has been stagnant for several quarters. The current price adjustment serves as a clearing mechanism for markets that had become detached from local income growth.

AlphaScala data currently tracks various sectors for volatility, including the Consumer Cyclical space where companies like Amer Sports, Inc. (AS stock page) maintain an Alpha Score of 47/100. While the housing market is distinct from retail consumer goods, the underlying theme of consumer caution and asset repricing remains a relevant component of broader stock market analysis. Investors should monitor how these real estate trends influence regional banking exposure, particularly for institutions with significant concentrations in commercial and residential real estate lending, such as those analyzed in our recent coverage of ServisFirst Bancshares.

The next concrete marker for this sector will be the upcoming release of regional inventory turnover data and updated mortgage delinquency reports. These filings will clarify whether the current price drops are attracting new buyers or if the market is entering a period of prolonged stagnation. Further adjustments in listing prices during the next fiscal quarter will provide the necessary evidence to determine if these valuations have reached a floor or if additional downside remains for the condo segment.