Cisco Systems product revenue climbed nearly 17% from a year earlier in the latest quarterly report, a pace that reverses several quarters of cautious enterprise hardware spending. The surge signals that corporate clients are starting to unlock IT budgets after a prolonged period of inventory digestion and delayed refresh cycles.

Three implications of the product surge:

- Enterprise network infrastructure spending is accelerating, led by campus switching and data center gear.

- A hardware-heavy revenue mix can compress gross margins, which typically run below Cisco’s software and services margins.

- Services and subscription revenue growth become the next benchmark; without them, the earnings beat may not translate into a higher valuation multiple.

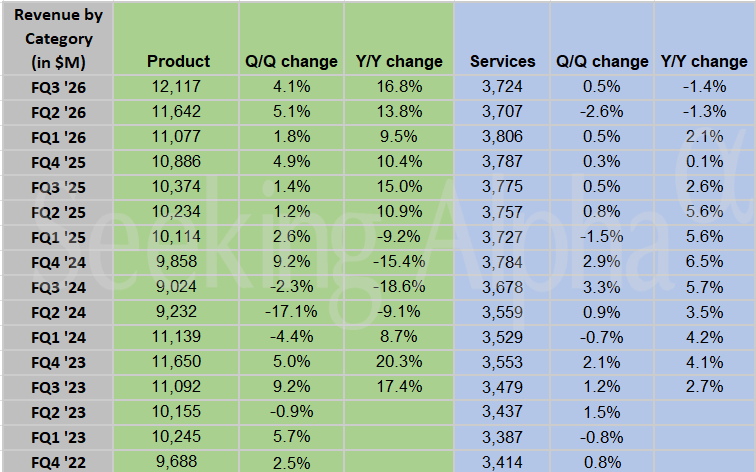

Product Revenue Spike Resets Cisco’s Demand Story

The near-17% leap in product sales is the strongest quarterly advance in the current cycle, according to charts released with the results. The company’s product category spans campus switching, data center switching, wireless, and security appliances – the core of its installed base. Charts from the earnings deck pointed to sequential order improvements across these segments, suggesting that large enterprises are no longer sitting on pandemic-era inventory but are actively refreshing their networks.

This shift matters because product revenue had been a drag on the stock for most of the past two years. The recovery implies that the replacement cycle for Wi-Fi 6E, 400G data center switching, and enterprise routing is finally materializing. For traders, the key question is whether this uptick is a one-time inventory catch-up or the start of a multi-quarter trend. The charts’ trajectory of order growth will be the most-watched indicator in the following quarters.

Hardware Mix Could Squeeze Margins, Shifting the Risk Equation

A product-led beat often comes with a profitability trade-off. Hardware revenue routinely carries lower gross margins than software licenses and services. Historically, Cisco’s product margins hover in the low 60% range while services top 65%. A quarter skewed toward product sales can therefore trim overall operating margins, even if the top line impresses.

Margin pressure would matter for a stock that has priced in a gradual shift toward a software and subscription model. If the product surge is not matched by solid services growth, the bottom-line impact may lag the revenue headline. Charts likely show deferred revenue and remaining performance obligations as leading indicators of future services traction. The sustainability of the product rebound will be judged by how quickly those software and services metrics follow.

What the Charts Mean for Cisco’s Next Catalyst

The stock’s post-print reaction will hinge on two factors: forward guidance on product order visibility and the pace at which large enterprise deals convert to services contracts. Charts tracking product backlog and annualized recurring revenue from software will be the clearest signal of whether the hardware spike is building a higher-quality revenue base.

For traders, the next concrete decision point is likely the company’s appearance at industry conferences where management can update the demand pipeline. A sustained product uptick would support a rerating of the stock out of the range it has occupied for much of the year. A stall, however, would confirm that the surge was a one-quarter inventory flush.

To stay current on enterprise technology moves, see our stock market analysis. For the execution tools to trade Cisco, check the best stock brokers.