Stocks● Neutral

Chromebook Q1 Shipments Fall 11%, GIGA Delay Threatens Recovery

Chromebook Q1 shipments fell 11% YoY as education demand stalled. Japan's GIGA School Program 2.0 delay removes the key catalyst. Vendor splits and timeline to watch.

Continue with

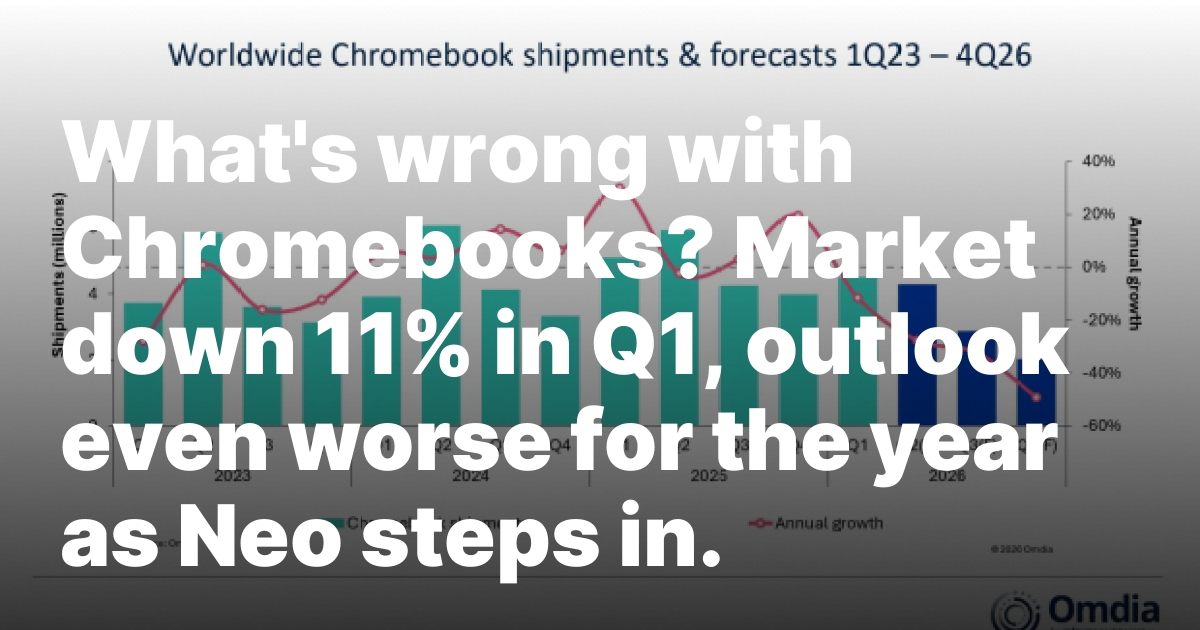

The Chromebook segment suffered an 11% year-on-year shipment decline in the first quarter of 2025, according to Omdia data. The drop is the steepest within the broader PC market, and the near-term outlook is worse. Japan's GIGA School Program 2.0, the category's most important upcoming procurement catalyst, faces supply-driven delays that could push orders into 2026. For investors tracking PC supply chains, the question is whether any substitute demand can fill the gap.

Japan's GIGA School Program 2.0 Sets the Next Catalyst

The first phase of the GIGA School Program 2.0, which ran from late 2024 through the end of 2025, completed without major disruption. That phase is now over. The second phase is deferred, with Kieren Jessop, Principal Analyst at Omdia, stating that supply constraints are likely to cause delays. Education-related deployments across other markets are also being postponed until conditions stabilize. For a category that depends almost entirely on government-funded school purchases, the pause creates a revenue vacuum. The single largest demand catalyst for Chromebooks – the GIGA program in Japan – is now uncertain on timing. If the second-phase tender slips past the second half of 2025, annual shipments could decline further.