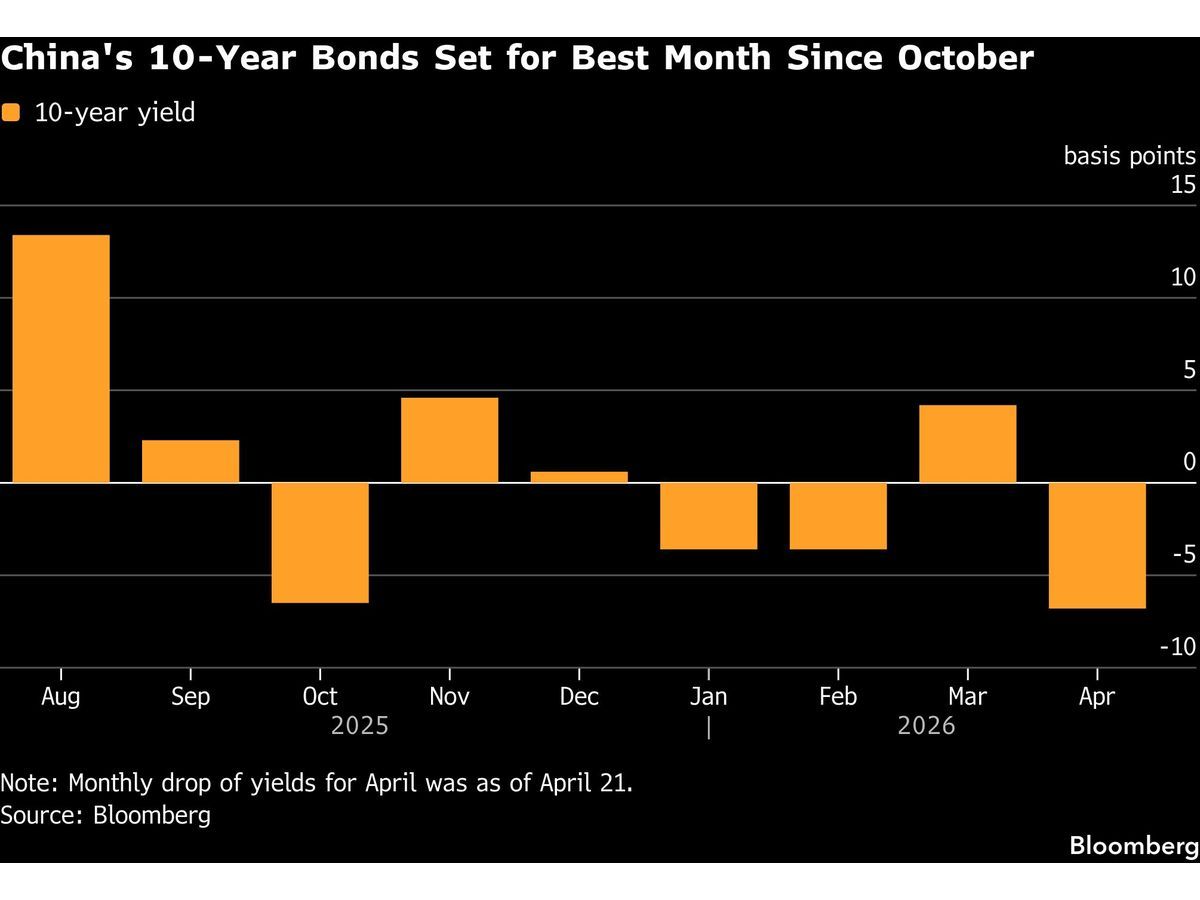

China’s benchmark bonds are currently tracking toward their strongest monthly performance since October. This rally persists despite ongoing concerns regarding the volume of upcoming government debt issuance. The market has prioritized the current abundance of liquidity over the potential for supply-driven volatility, suggesting that institutional demand remains robust in the face of broader macroeconomic uncertainty.

Liquidity Dynamics and Debt Supply

The current strength in the sovereign bond market reflects a disconnect between fiscal supply schedules and monetary conditions. While the market anticipates a significant increase in debt issuance, the central bank has maintained a supportive stance that keeps short-term funding costs manageable. This liquidity cushion has allowed investors to absorb new bond offerings without forcing a meaningful repricing of yield curves. The persistence of this trend indicates that the prevailing appetite for fixed income remains anchored by the availability of cash rather than immediate fiscal concerns.

Sectoral Read-Through and Market Positioning

This bond market activity provides a critical signal for broader asset classes, particularly as investors weigh the stability of the Chinese financial system against global interest rate trends. When liquidity conditions remain loose, the pressure on equity valuations in sectors like technology and consumer cyclicals often eases. For instance, companies such as ON Semiconductor Corporation or Amer Sports, Inc. operate within environments where capital costs and liquidity availability dictate expansion capacity. AlphaScala currently assigns a Mixed label to both ON and AS, reflecting the volatility inherent in their respective sectors during periods of shifting monetary policy.

AlphaScala Data Context

Our internal metrics reflect a nuanced landscape for industrial and consumer-facing equities. While AGILENT TECHNOLOGIES, INC. holds a Moderate Alpha Score of 55/100, the broader technology and consumer sectors continue to navigate the ripple effects of regional liquidity shifts. These scores are derived from current market data and provide a baseline for assessing how individual firms respond to the macro environment described above.

The Path to Policy Clarity

The next concrete marker for this bond rally will be the official data release regarding the pace of local government special bond issuance. If the actual supply hits the upper end of market estimates without a corresponding tightening of interbank rates, the current rally may face a test of its durability. Investors are now looking for the central bank to clarify its stance on liquidity management for the upcoming quarter, as any shift in the tone of open market operations will likely dictate whether the current bond momentum can be sustained into the next cycle. The interplay between fiscal issuance schedules and central bank intervention remains the primary variable for the remainder of the quarter.