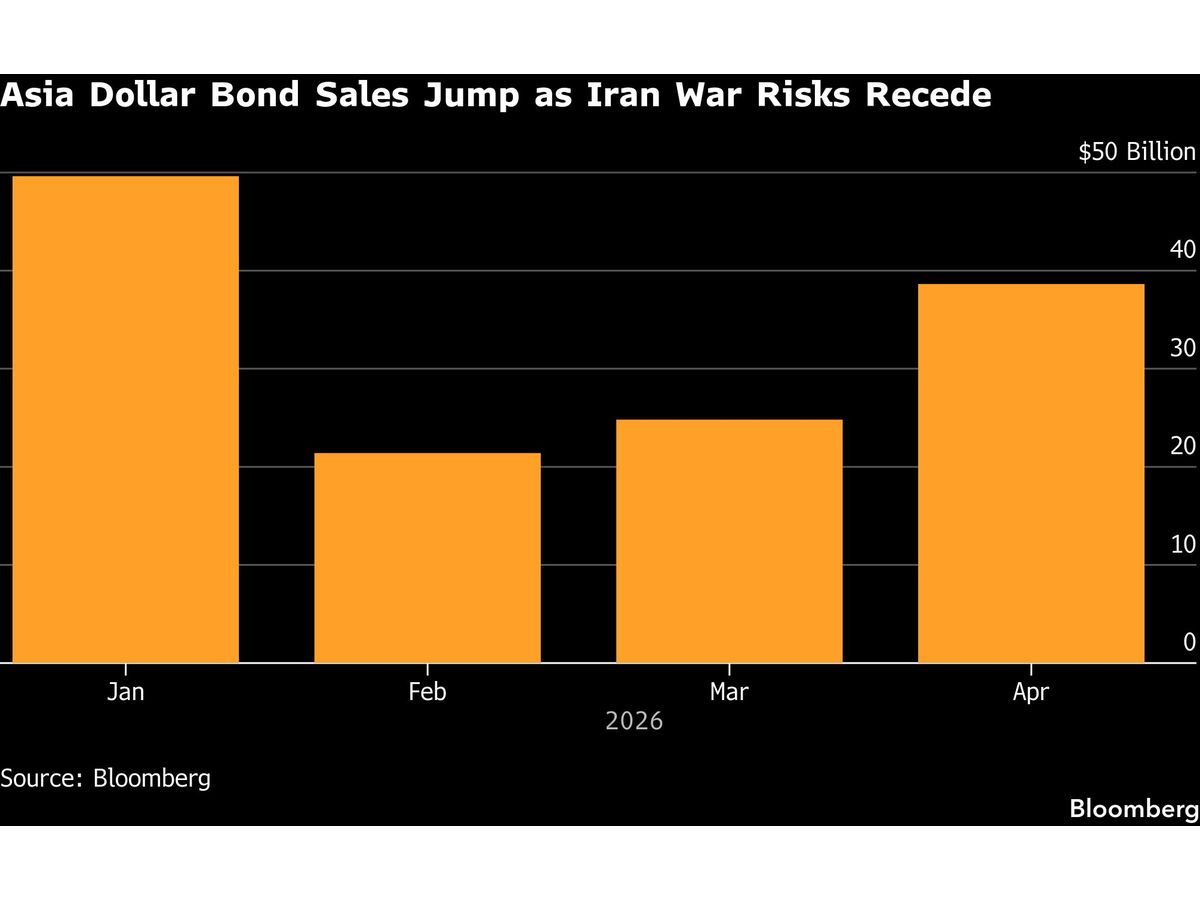

The Asia-Pacific dollar bond market experienced a significant shift in April, recording $38 billion in new offerings. This figure represents the highest issuance volume for the month of April since 2021, marking a sharp recovery from the $22 billion recorded in March. The primary driver behind this surge was a temporary stabilization in geopolitical conditions following the start of a ceasefire in the Iran war, which allowed regional borrowers to return to the debt capital markets with renewed urgency.

The Mechanics of the Issuance Rush

The 67% year-on-year increase in issuance volume signals more than a simple catch-up on delayed funding. Regional borrowers are actively seeking to diversify their capital structures, utilizing dollar-denominated debt to hedge against potential future geopolitical volatility. As noted by Daniel Kim, head of debt capital markets for Asia at HSBC Holdings Plc, the current environment is defined by a narrow window of opportunity. Issuers are prioritizing speed to market, anticipating that the current period of relative calm may be transient. This behavior is consistent with broader stock market analysis regarding how credit markets react to sudden geopolitical lulls.

Regional Concentration and Credit Quality

The surge in activity was not evenly distributed across the region. Japan, Australia, and South Korea dominated the landscape, collectively accounting for 78% of the total issuance volume in April. This concentration reflects a distinct flight-to-quality preference among investors. In periods of uncertainty, capital flows toward the most stable, high-grade issuers first, while lower-rated borrowers face a more difficult path to market access. This hierarchy is expected to persist as long as the underlying geopolitical situation remains fragile.

Valuation and Yield Compression

The appetite for Asian credit has reached a point where the average yield premium for investment-grade dollar debt has hit a record low. This tightening of spreads indicates that investors are currently willing to accept minimal compensation for credit risk in the region. While this environment is favorable for issuers looking to lock in lower borrowing costs, it also leaves little room for error should market conditions deteriorate. The current valuation levels suggest that the market is pricing in a sustained period of stability, which may be vulnerable to any disruption in energy flows or a breakdown in the current Middle East truce.

Operational Risks and Future Volatility

For market participants, the primary risk remains the fragility of the current ceasefire. As Rishi Jalan, head of Asia debt syndicate at Citigroup Inc., noted, issuers exposed to higher oil prices face the risk of seeing their borrowing premiums widen rapidly if energy markets are disrupted. The strategy for many firms has shifted toward extreme agility, with issuers maintaining readiness to tap the market at a moment's notice. This operational posture is a direct response to the reality that windows for issuance can close as quickly as they open.

While the year-to-date volumes are now broadly flat compared to the previous year, the underlying sentiment is highly sensitive to external shocks. Investors should monitor the stability of energy prices and the duration of the current geopolitical truce as primary indicators for future issuance viability. Should the ceasefire fail, the cost of capital for energy-sensitive Asian economies is likely to rise, potentially forcing a retreat from the dollar bond market and a widening of credit spreads across the region. For those tracking broader industrial trends, the FAST stock page and KIM stock page provide additional context on how industrial and real estate entities are navigating these shifting capital environments, with Alpha Scores of 53 and 55 respectively indicating a mixed to moderate outlook for these sectors.