The Iran war has forced analysts to flag extreme bearish scenarios for three of Asia's most oil-dependent economies. India's rupee could weaken to 100 per dollar, Indonesia's rupiah to 18,000, and the Philippine peso to 65 as crude prices surge more than 40% since the conflict began in late February.

The three currencies have already fallen between 4.5% and 6.5% since the war started. The pressure stems from widening current-account deficits, rising inflation expectations, and higher US Treasury yields that make emerging-market assets less attractive. The pain is most acute in net oil importers that rely on foreign capital.

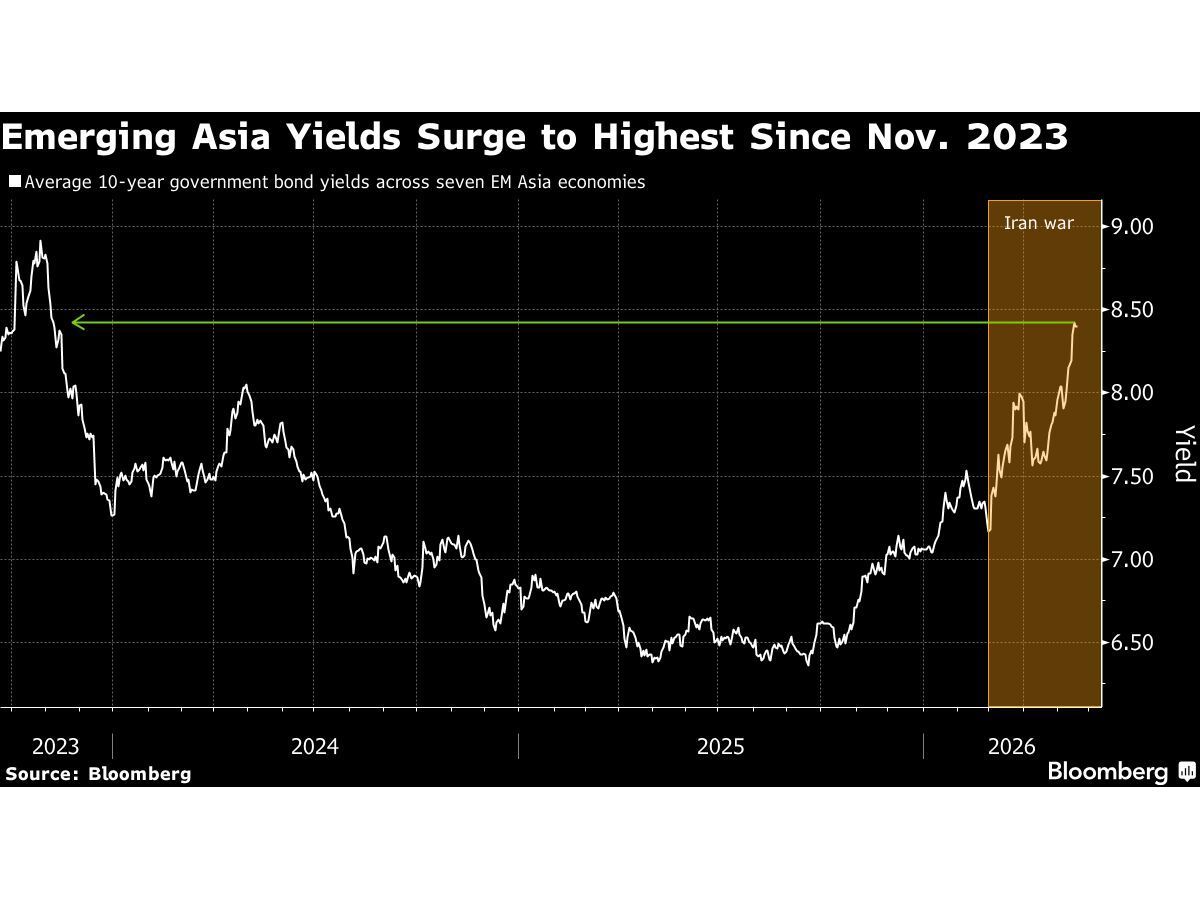

“The deterioration in import costs relative to export prices will continue to weigh on the currencies of net oil importers” if energy prices continue to rise, said Rajeev De Mello, global macro portfolio manager at Gamma Asset Management SA. Higher crude prices may also hurt bonds, as they stoke inflation or widen fiscal deficits where authorities absorb part of the shock through fuel subsidies.

Rupee: 100 in the Forward Market Already

Aberdeen Investments and MetLife Investment Management are among those that see the possibility of the rupee weakening to 100 per dollar. DBS Group Holdings has revised its forecast range to 95-100 from 90-95. The consensus estimate compiled by Bloomberg shows 94.75 by year-end. The one-year dollar-rupee forward breached 100 for the first time on Wednesday.

Forecast Revisions Stack Up

Key data points:

- DBS rupee forecast range: 95-100 (from 90-95)

- Consensus year-end estimate: 94.75

- One-year forward: breached 100 on Wednesday

- Rupee depreciation since war: about 5.5%

What Would Confirm a Break

The forward market already prices in a weaker rupee than the consensus. A spot break above 95 would trigger stops and accelerate toward the 100 level. The trigger would be crude prices staying above $100 per barrel for several more weeks, which would widen the trade deficit and force the Reserve Bank of India to choose between draining reserves and allowing a sharper depreciation.

Rupiah: Hawkish Rate Hike Meets Persistent Pressure

Indonesia's central bank surprised markets on Wednesday with a larger-than-expected rate hike and a pledge to step up currency intervention. The rupiah has continued to weaken. BNY Mellon strategist Wee Khoon Chong wrote in a May 13 note that the rupiah could slide to 18,000 in the near term. HSBC Holdings now expects the rupiah to end the year at 17,400, up from its previous estimate of 17,300. The Bloomberg consensus stands at 17,100.

BNY Mellon's 18,000 Near-Term Target

Key data points:

- BNY Mellon near-term target: 18,000

- HSBC year-end forecast: 17,400 (from 17,300)

- Consensus year-end estimate: 17,100

- Rupiah depreciation since war: about 6%

The Policy Quandary: Export Controls and Capital Flight

President Prabowo Subianto on Wednesday announced plans to tighten state control over commodity exports. He estimates the country loses as much as $150 billion annually through “leaks” such as under-invoicing, where exporters fail to declare the full value of shipments. The move signals growing policy intervention as the currency weakens. It also creates uncertainty for foreign investors already wary of governance risks. Rate hikes alone may not stem capital outflows if global risk appetite shrinks further. Indonesia's reliance on foreign portfolio inflows to fund the current-account deficit makes it vulnerable to any spike in US Treasury yields.

Peso: 65 and 8% – A Double Squeeze

The Philippine peso has depreciated about 4.5% since the war began. Gamma's De Mello said the peso could weaken beyond 65 if oil prices continue to climb. HSBC revised its year-end peso forecast to 60.8 from 59.8. The Bloomberg consensus stands at 60.3.

Bond Yields at Multi-Year Highs

The head of the money market association in the Philippines said yields may climb toward 8%, a multi-year high. Rising inflation expectations and currency depreciation push foreign investors to demand higher compensation for risk. Higher yields impose a drag on the government's budget through increased borrowing costs.

The Oil Mechanism: Crude Dependency and Capital Flow Risks

India, Indonesia, and the Philippines are all net oil importers with persistent current-account deficits. The table below shows the three currencies' depreciation since the war and the bearish targets compared with consensus:

| Currency | Bearish Target | Consensus Year-End | Depreciation Since War |

|---|

| INR | 100 | 94.75 | ~5.5% |

| IDR | 18,000 | 17,100 | ~6% |

| PHP | 65 | 60.3 | ~4.5% |

Why These Three Economies Bleed

Each country imports a significant share of its crude. Higher energy costs widen trade gaps and stoke inflation. Rising US Treasury yields further dent the appeal of emerging-market assets, pressuring central banks to tighten policy even as the economic fallout from the conflict deepens. The countries rely on foreign capital to fund their deficits. When that capital flows out, currencies fall and bond yields rise in a self-reinforcing cycle.

Next Catalyst: Oil Above $100 and Central Bank Credibility

Oil prices remain the primary trigger. Each successive week of elevated crude prices raises the probability that these extreme scenarios become the consensus rather than tail risks. A sustained break above $100 per barrel would likely push more analysts to adopt the 100/18,000/65 targets as base cases.

The next concrete marker is the path of spot currency levels. If India's rupee breaks above 95 in the spot market, the 100 target becomes the path of least resistance. For Indonesia, a spot rupiah above 17,500 would put the 18,000 level in play. For the Philippines, a break above 61 would signal a move toward 65.

Central bank credibility is the other variable. Indonesia has already hiked rates and signaled further intervention. India has not yet moved aggressively. The market will watch whether the Reserve Bank of India allows a controlled depreciation or draws down reserves to defend 95. Either outcome moves the currency closer to the extreme scenarios.

For a broader view of how risk-off sentiment affects global indices, see our stock market analysis page.

The Iran war has no clear end date. Until crude prices stabilize or reverse, the pressure on these currencies and bonds will intensify. The extreme scenarios are no longer unthinkable – they are being priced in by the forward market and acknowledged by a growing list of asset managers and banks.