Stocks● Neutral

The Stethoscope Took Decades. Markets Miss the Same Pattern.

A systematic scan of invention timelines reveals a recurring pattern: some technologies arrive decades after their prerequisites are in place. That feasibility gap is a market blind spot that can reprice entire sectors when the bottleneck breaks.

Continue with

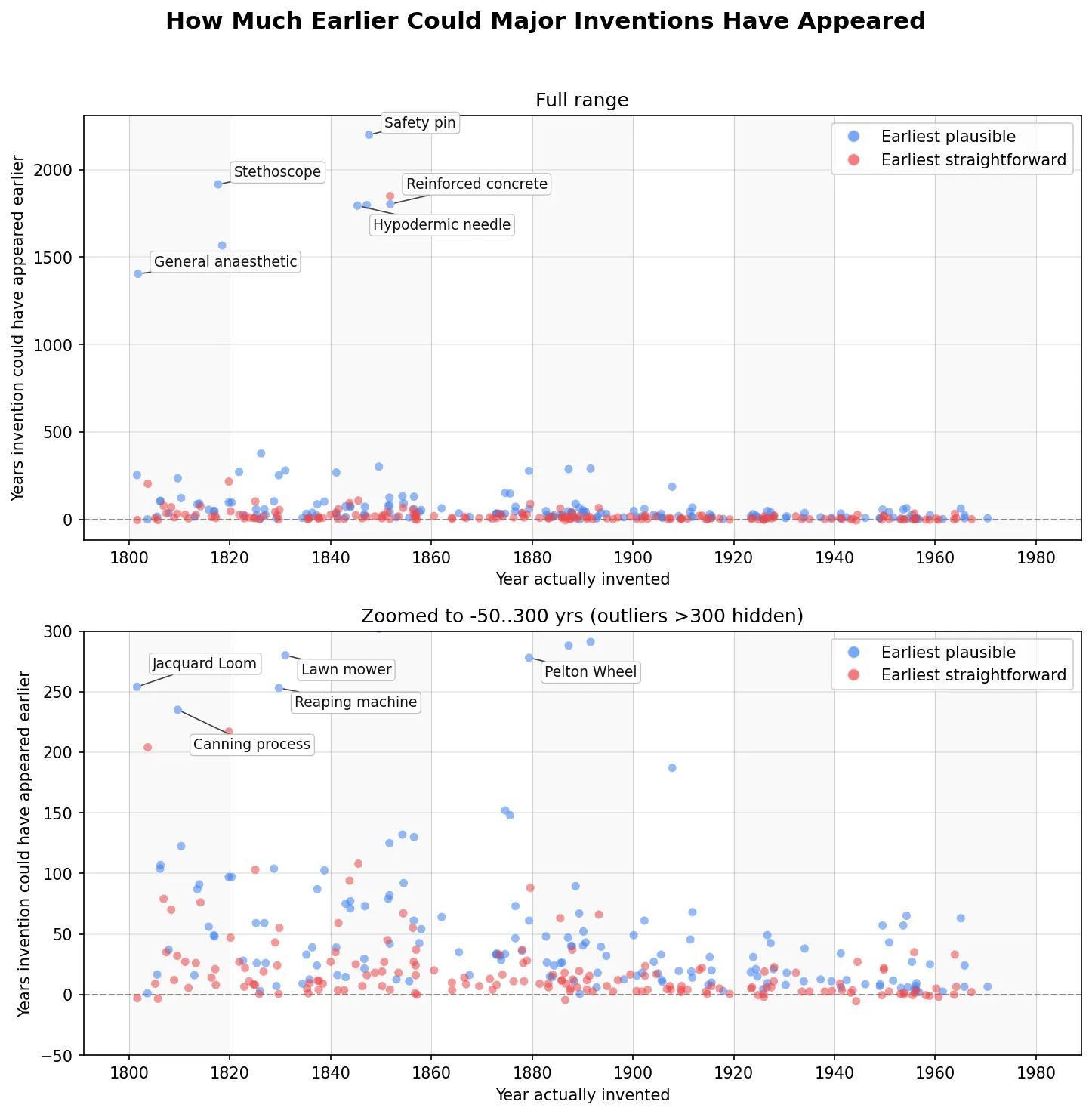

A systematic scan of invention timelines shows that most useful technologies appear almost as soon as they become physically possible. The airplane, for example, needed a high power-to-weight engine, which arrived around 1880; the Wright brothers flew in 1903, just behind the earliest feasible date. That pattern holds for many breakthroughs. A small set of ideas, however, arrived decades or even centuries after their prerequisites were in place. The stethoscope, general anesthesia, reinforced concrete, the Jacquard loom, and canning all fall into this category. The lag is not a historical curiosity. It is a recurring market blind spot that leaves entire sectors underpriced relative to their sudden-acceleration potential.

The Feasibility Gap and Why It Matters for Equity Valuation

When an invention is physically possible but not yet commercialized, the missing ingredient is rarely a single missing part. It is usually a failure of imagination, a regulatory block, or an incumbent’s quiet suppression of a competing standard. The stethoscope required only a rolled paper tube–available for centuries before René Laennec’s 1816 device. General anesthesia needed gases already known in the 1700s, yet surgery without agony did not spread until the 1840s. Reinforced concrete waited until the late 19th century despite iron and concrete both being ancient materials.

For an equity analyst, the feasibility gap is a valuation variable. A sector where the technical building blocks are in place but adoption is stalled trades at a discount that can evaporate in a single product cycle. Medical devices, for example, still contain procedures that rely on manual skill when sensor fusion and robotics could automate them. The building materials sector uses supply chains that have not fundamentally changed in 50 years, even as material science has advanced. The gap between what is possible and what is listed on a balance sheet is a source of mispricing.

Canning, Jacquard, and the Industrial Pattern of Delayed Adoption

Canning took decades to spread after Nicolas Appert’s 1810 method, not because glass jars were expensive but because the military procurement system that needed it was slow to reorder supply chains. The Jacquard loom, a punch-card-controlled weaving machine invented in 1804, faced violent resistance from silk workers who saw it as a threat to their craft. The technology worked; the social and organizational systems did not adapt until much later.

The same pattern shows up in modern markets. Building information modeling software can cut construction waste by 20% or more, yet adoption among small and mid-sized contractors remains low because the industry’s fragmented structure rewards short-term cost avoidance over long-term productivity. Telemedicine infrastructure was technically ready a decade before the pandemic forced reimbursement codes to change. The catalyst was not a new invention; it was a regulatory and behavioral shift that unlocked a pre-existing capability.