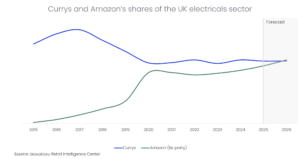

Amazon is on track to overtake Currys as the UK's largest electricals retailer by first-party sales, according to GlobalData. The research group's forecast puts Amazon's own-brand and direct-sourced electricals revenue ahead of Currys' total electricals sales within the next two years.

Currys, which trades from roughly 300 stores across the UK and Ireland, has held the top spot for years. The shift marks a milestone in the slow erosion of traditional retail share by the e-commerce giant.

The projection covers Amazon's first-party sales only–items Amazon buys, stocks, and sells directly. Third-party marketplace sales are excluded. That distinction matters because it shows Amazon building inventory and logistics muscle specifically in the electricals category, not just acting as a platform for other sellers.

GlobalData analyst Patrick O'Brien said the challenge for Currys is acute. “Currys loses on price, convenience and speed of delivery,” he said. “The one area it can still compete is in-store experience.” O'Brien argues that Currys must lean into services that online-only models cannot easily replicate: live product demonstrations, setup assistance, extended warranties with face-to-face support, and instant “take it home” fulfilment for certain items.

The read-through for the broader UK electricals sector is straightforward. Any retailer that competes in white goods, consumer electronics, or home-office gear faces the same pressure. Amazon’s first-party expansion drags down margins systemically because it squeezes pricing power. Smaller chains and pure-play online rivals that lack Currys' store count or service infrastructure are even more exposed.

Physical retailers across the sector are fighting for relevance. Dixons Carphone–the parent of Currys and the Carphone Warehouse brand–brought in new management two years ago to refresh the store format and push higher-margin services. The pandemic accelerated online adoption, and the recovery did not send shoppers back to stores at pre-2020 rates. GlobalData's data shows that UK electricals spend has shifted roughly 60-40 online to offline, a split that continues to tilt.

For traders tracking UK retail stocks, the trajectory is clear even if the timing is uncertain. Currys' shares have lagged the FTSE 250 over the past three years. The company's enterprise value trades at a discount to net tangible assets, partly because the market prices in further share loss to Amazon. Rivals like AO World, which focuses on appliances, and Argos, owned by Sainsbury's, face similar structural headwinds. AO World's share price has rebounded from pandemic lows but still sits well below its 2018 peak.

The key variable is execution. GlobalData's view is not that Currys is doomed. It is that Currys must transform its store estate from a place to buy products into a place to solve problems. That means staff training, inventory systems that can match online availability, and a service layer that feels worth the premium. If Currys succeeds in that, it can hold a profitable niche. If it drifts, Amazon will take the rest.

O'Brien's comment on in-store experience is not new–the strategy has been discussed in retail circles for years. What is new is the clock. The forecast gives Currys a narrow window before Amazon's scale makes the gap too wide to close. The next few quarters will show whether management can move fast enough to slow the shift.

The September trading update from Currys will offer the first hard data point. Same-store sales, service revenue growth, and online mix will be the numbers to watch.