Stocks● Neutral

AI Liability Risks Force Insurers to Define Coverage Limits

AI-driven litigation is forcing insurers to determine if algorithmic risks are insurable, creating a new financial hurdle for companies deploying AI systems.

Continue with

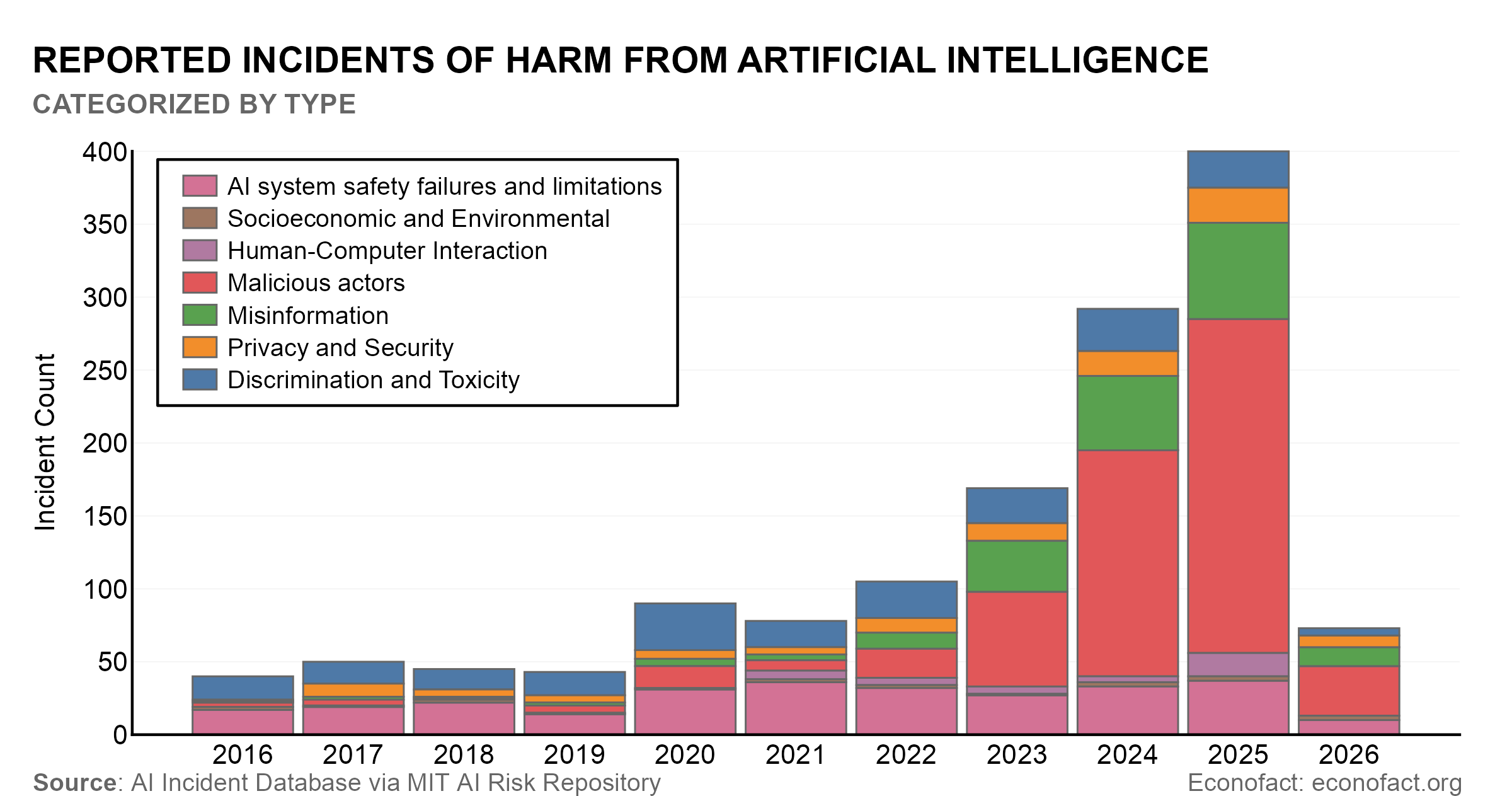

The rapid integration of artificial intelligence into commercial operations has created a new class of legal and financial exposure that traditional insurance models are struggling to quantify. As AI systems take on more autonomous decision-making roles, the resulting lawsuits are expanding in both frequency and legal complexity. This shift forces a fundamental question for developers and operators: whether the liability associated with AI-driven outcomes can be effectively transferred to insurers or if the risks are becoming too unpredictable to underwrite.

The Mechanism of AI Liability Exposure

The core problem for insurers lies in the lack of historical data to price AI-related risk. Unlike established sectors where actuarial tables provide a clear path to premium calculation, AI systems operate in a landscape of evolving legal precedents. When an AI model produces a faulty output that results in financial loss or legal damages, the chain of responsibility is often obscured between the developer, the operator, and the end-user. This ambiguity makes it difficult for insurance companies to determine which party bears the primary burden of liability, potentially leading to a coverage gap that leaves companies exposed to significant capital impairment.