An analyst upgraded Advanced Micro Devices after the company reported a Q1 that delivered solid execution and robust topline growth. The upgrade shifts the risk/reward profile. The real question is whether the growth can sustain.

The simple read is straightforward: AMD executed well, the product cycle is strong, and the upgrade validates the momentum. For a trader scanning headlines, that is the takeaway. The better market read requires a closer look at what the upgrade actually prices in and what could break the setup.

The Upgrade and Its Simple Case

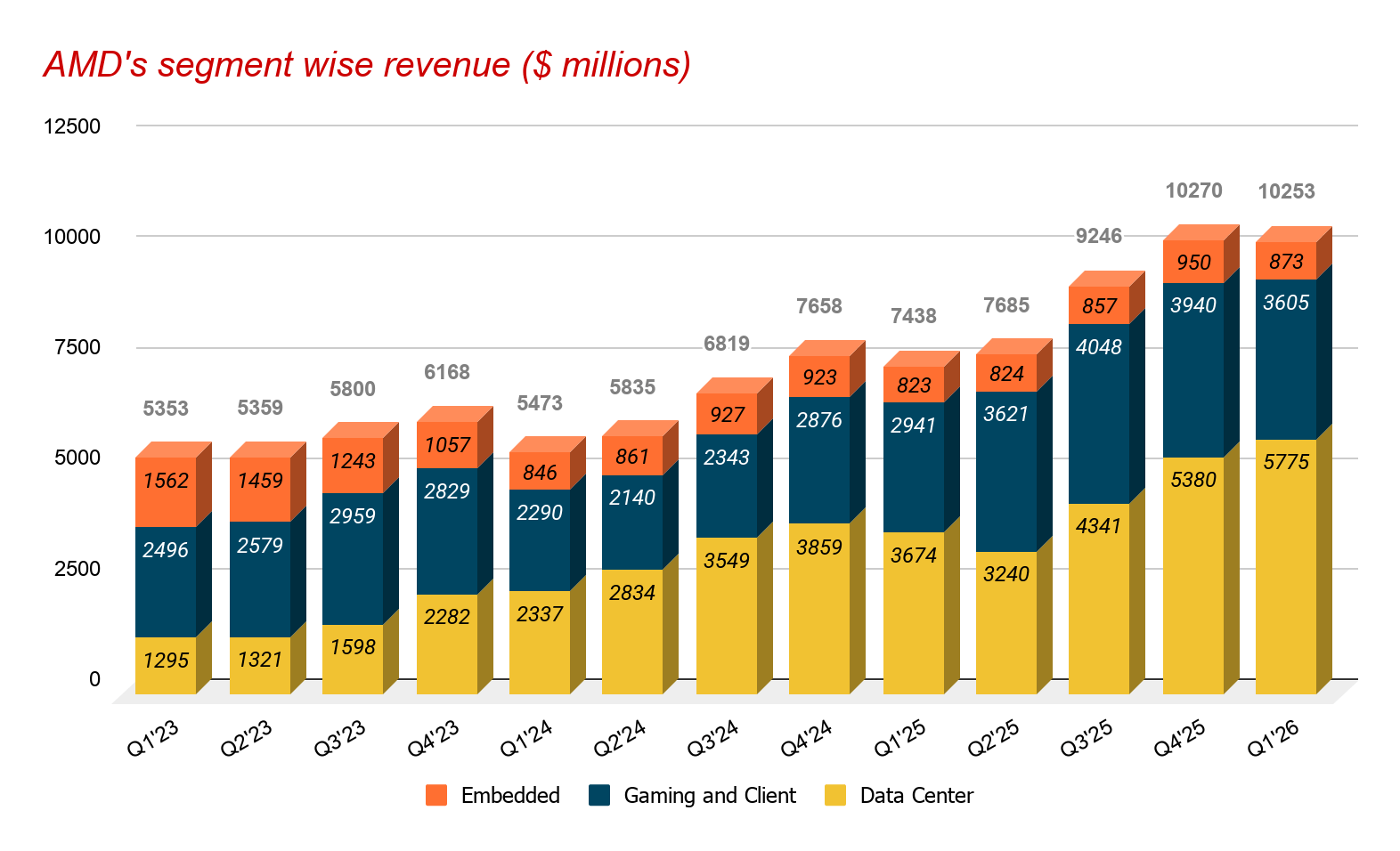

The upgrade followed a quarter driven by demand for EPYC server CPUs and Instinct AI accelerators. EPYC is gaining share in the server CPU market. Enterprises are refreshing data centers and choosing EPYC. Instinct, AMD's line of AI accelerators, is the higher-growth driver, competing directly with Nvidia in the training and inference segments.

The Q1 report delivered a revenue beat and improved visibility into the pipeline. The analyst upgrade suggests confidence that AMD can maintain or accelerate that growth. Competitive pressure, however, is intense. Nvidia's Blackwell platform and custom ASICs from cloud hyperscalers pose real threats. If AMD's Instinct adoption slows or if EPYC share gains plateau, the upgrade would look premature.

The Competitive and Demand Risk Behind the Upgrade

The upgrade assumes that EPYC and Instinct demand is durable. A reduction in risk would come from concrete signals that demand is accelerating. A guidance raise in the next quarter, expansion of Instinct design wins beyond the current hyperscaler customers, or a clear path to margin expansion would all support the upgraded thesis.

The risk increases if any of the following materialize:

- A miss on Q2 guidance

- A slowdown in AI spending by major cloud providers

- A competitive product launch from Nvidia that erodes Instinct's value proposition

A broader macro downturn that pushes enterprise IT budgets lower would also hurt AMD disproportionately given its premium valuation.

Valuation and the Decision Point in Q2

After the upgrade, AMD's valuation is a key variable. The stock trades at a premium to historical multiples, reflecting the AI growth premium. That premium is justified only if AMD delivers consistent beats and raises guidance. Execution risk is non-trivial: supply chain constraints, wafer allocation, and the ramp of new products all factor into the next quarter's results.

AlphaScala's proprietary model assigns AMD an Alpha Score of 59 out of 100, a Moderate rating. That score reflects balanced risk/reward after the upgrade, neither screaming buy nor obvious sell. The model weighs the strong product cycle against valuation and competitive pressure.

The next concrete catalyst is the Q2 earnings report, where management will provide guidance. The market will watch for the trajectory of Instinct revenue and any commentary on the MI400 next-generation accelerator. A beat and raise would confirm the upgrade. A miss would reverse it quickly.

For traders tracking the stock, the AMD stock page on AlphaScala provides real-time data and sentiment. The broader market analysis section offers context on how semiconductor names are pricing in the AI cycle. The upgrade changes the setup. The next quarter will decide whether it was a turning point or a peak.