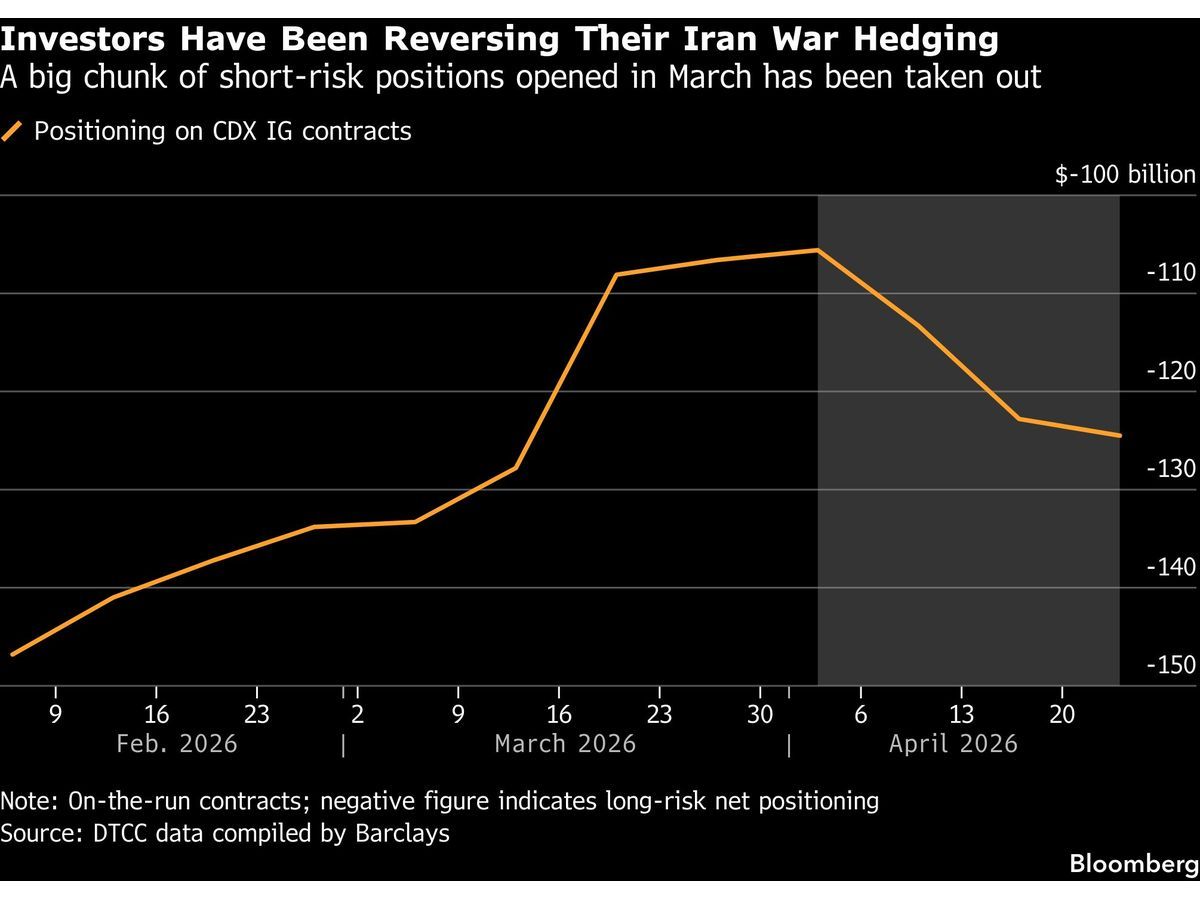

Aegon Asset Management and Barclays Plc have issued warnings that the credit rally observed throughout April may be nearing an abrupt conclusion. The shift in sentiment suggests that the recent momentum in credit markets is vulnerable to a rapid reversal as liquidity conditions tighten and investor risk appetite wanes.

Vulnerability in Credit Markets

The current market environment reflects a disconnect between prevailing asset prices and underlying macroeconomic pressures. Analysts at both firms point to the speed of the April gains as a primary concern. Rapid appreciation in credit valuations often leaves portfolios exposed when market participants begin to prioritize capital preservation over yield chasing. This caution is particularly relevant for institutional investors who have relied on the recent rally to bolster quarterly performance metrics.

Sector Read-Through and Valuation

Financial services firms are often the first to feel the impact of shifting credit cycles. Barclays, which maintains an Alpha Score of 59/100, reflects a moderate outlook within the broader financial services sector. Investors monitoring these developments should examine the BCS stock page for further updates on how the firm is positioning its balance sheet against potential volatility. The broader stock market analysis suggests that the sustainability of credit spreads remains the most critical variable for the remainder of the quarter.

The Catalyst Path

The next concrete marker for this narrative will be the upcoming round of central bank commentary and regional economic data releases. If credit spreads begin to widen, it will serve as a confirmation that the April rally has exhausted its fundamental support. Market participants are now looking for signs of institutional selling or a reduction in risk-weighted assets as the primary indicator of a broader trend reversal. The transition from a period of aggressive buying to defensive positioning will likely be defined by how quickly liquidity dries up in secondary credit markets.