Back to Markets

Stocks● Neutral

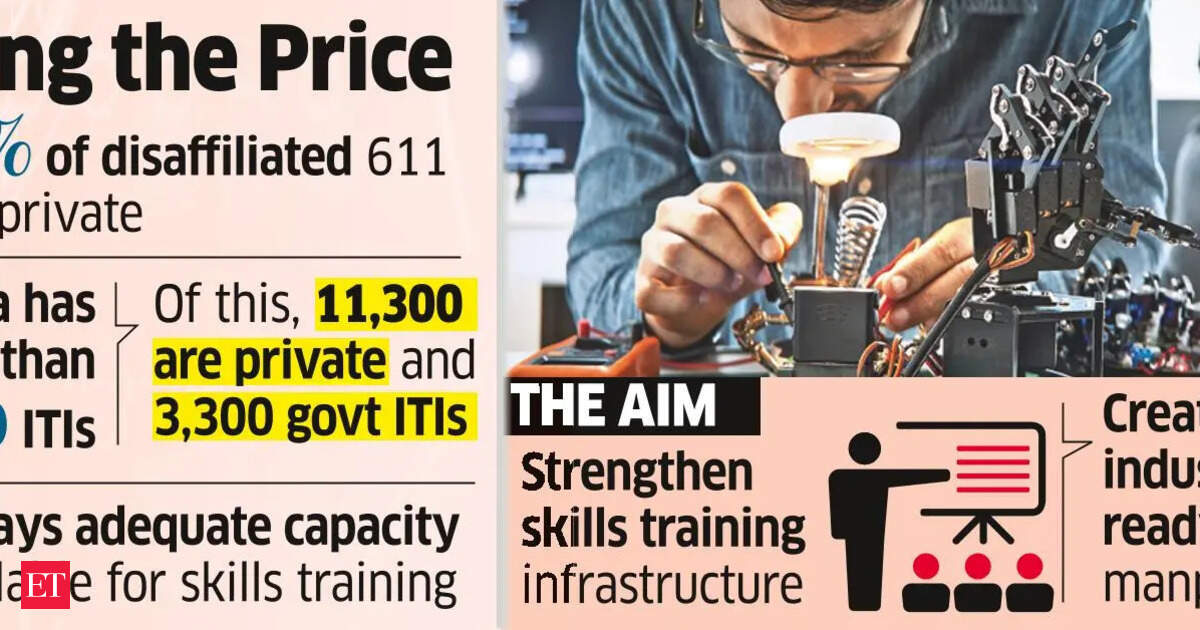

611 ITIs Stripped of Affiliation in Skills Sector Clean-Up

India disaffiliates 611 ITIs with zero admissions from 2022-2025. A compliance shift that consolidates the sector toward active operators across 20 lakh available seats.

Continue with

The government's decision to disaffiliate 611 Industrial Training Institutes (ITIs)–22 government-run and 589 private–sets a new baseline for the skills training sector. The margin note is the cause: these institutes recorded zero student admissions and were effectively non-operational between 2022 and 2025.

The read-through is not about a supply shock. The 20 lakh seats that remain available nationwide tell the story of excess capacity, not constraint. What changed is the signal the regulator sent about compliance and data integrity.

What the Disaffiliation Actually Changes

The immediate consequence is a cleaner dataset. The National Council for Vocational Education and Training (NCVET) or the relevant state directorates lose the noise of phantom seats in their official tallies. For a chain operator or a single-site ITI that is actually running classes, the competitive dynamic shifts marginally–fewer paper entities soaking up potential student inquiries or government scheme allocations.

Mechanism: Government schemes like the Pradhan Mantri Kaushal Vikas Yojana (PMKVY) often use ITI affiliation as a gate for funding or placement-linked bonuses. A disaffiliated ITI cannot claim those funds. The state-level Directorate of Training also reclaims the ability to audit and inspect against real attendance instead of a zero-admission facility.

Risk to watch: The operational gap between 2022 and 2025 means these 611 ITIs have already been idle for three academic cycles. The disaffiliation formalizes what was already true. There is no surprise for existing students or creditors–there were none.

Sector Read-Through: Private ITI Operators Feel the Pinch

The 589 private ITIs in the disaffiliation pool represent the bulk of the cancellations. Private ITIs operate on thin margins and are heavily dependent on government affiliation for legitimacy and student enrollment. A disaffiliated private ITI loses access to central and state training grants, placement-linked incentives, and the ability to issue NCVT-recognized certificates.