Stocks● Neutral

Why the Biggest Unicorns Face a Public-Market Reality Check

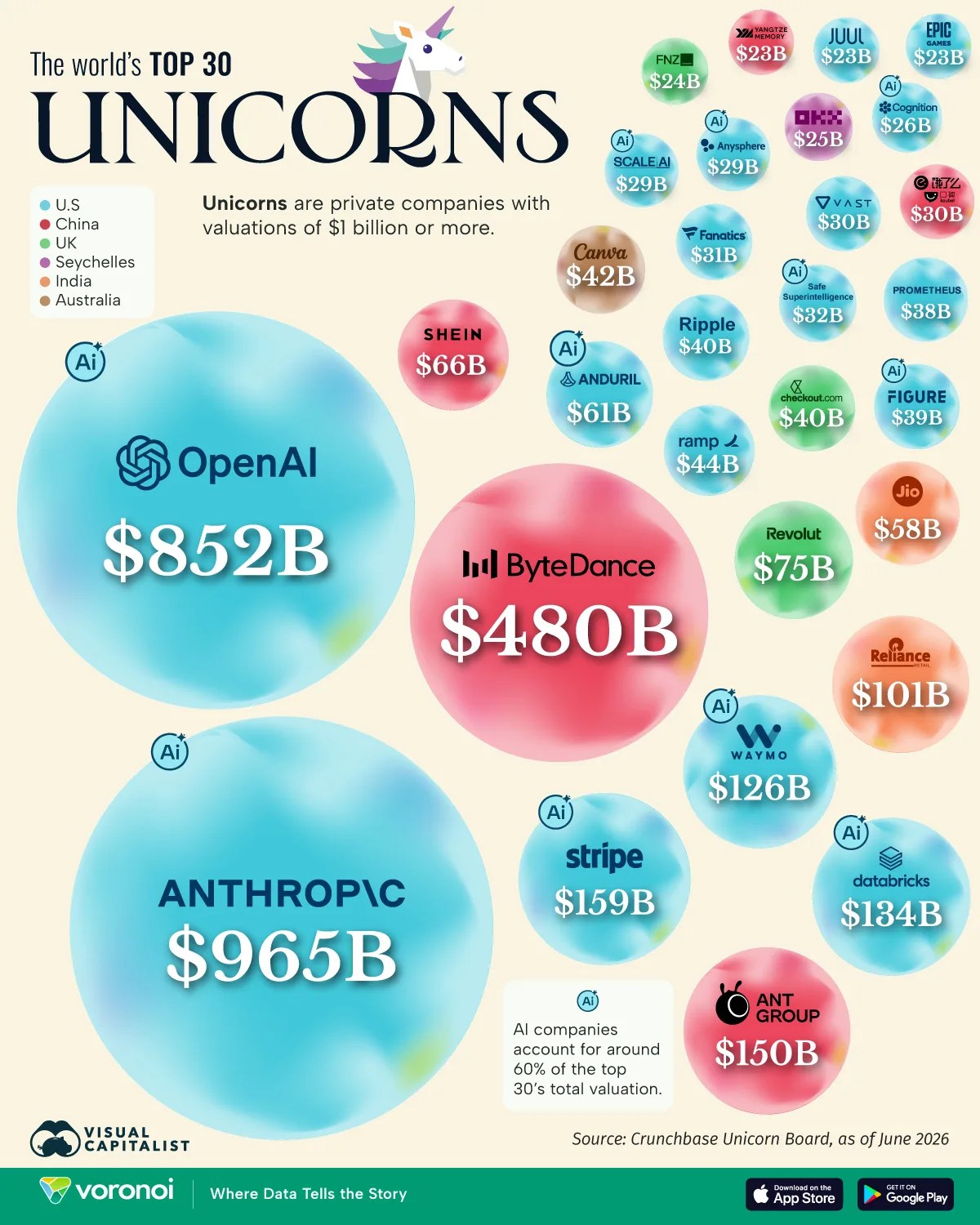

ByteDance leads at $225 billion. SpaceX, Stripe, Shein, and Databricks follow. The IPO window is open for some sectors. Timing will decide which unicorns keep their private valuations.

Continue with

ByteDance leads the global unicorn ranking at $225 billion. SpaceX follows at $150 billion. Stripe, Shein, and Databricks round out the top five. All are private companies worth $1 billion or more that have never sold a share on a public exchange.

The list is long. The valuations are large. The waiting game is the story.

Rudiger Dornbusch once said things take longer to happen than you think they will, then happen faster than you thought they could. That quote fits the unicorn cohort right now. For years, investors watched these companies accumulate private capital, delay IPOs, and push the boundaries of what a private market can hold. The slow phase has lasted a long time.

The Dornbusch turning point may be close. A handful of the biggest names – the payments processors, the rocket builders, the enterprise software platforms – have been preparing for public listings. Their private valuations reflect optimism that may or may not survive the scrutiny of quarterly earnings calls. The gap between private and public pricing is the risk.