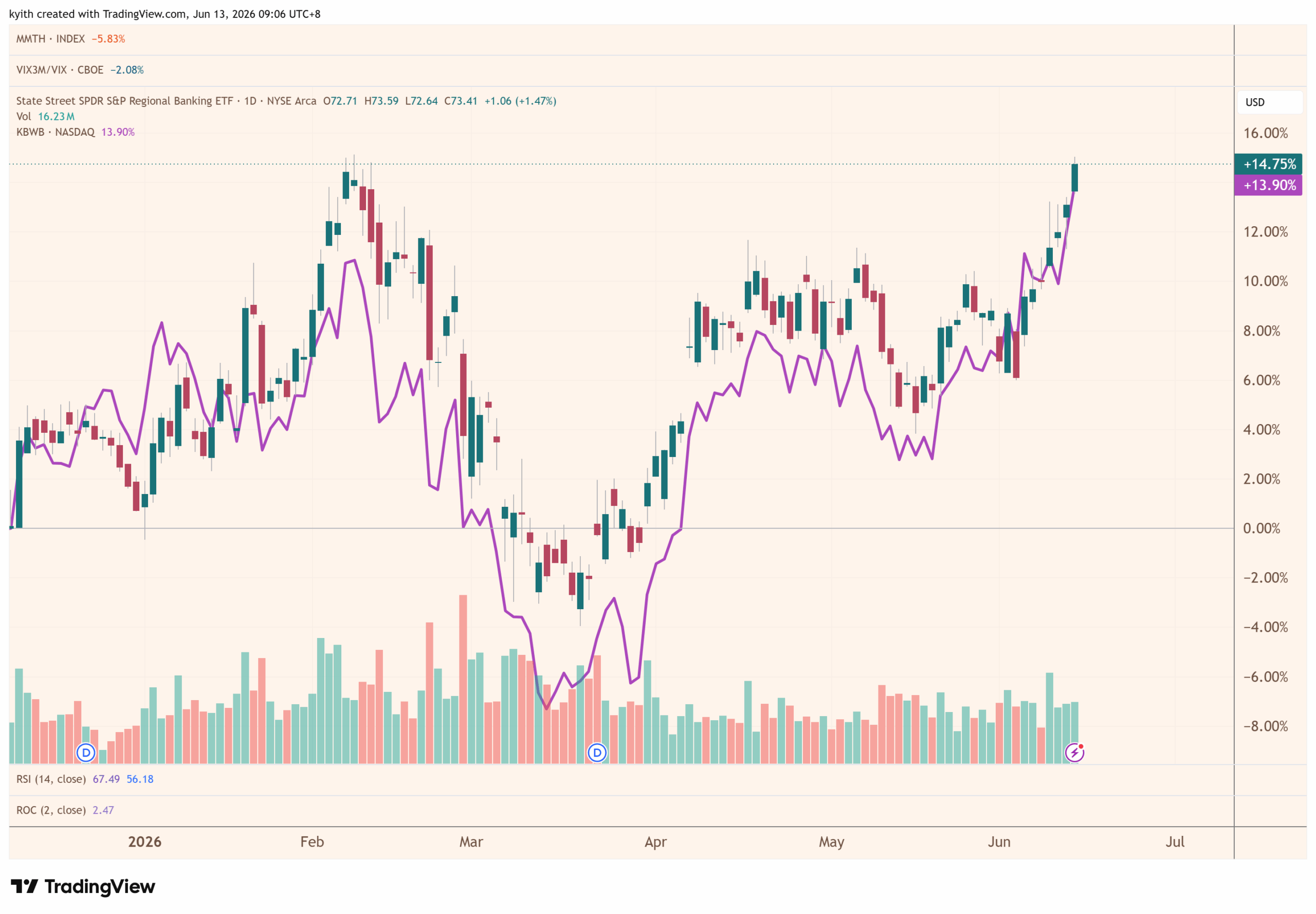

The KRE regional bank ETF has rallied 7.9% in two weeks. The yield curve flattened over the same period. Rates moved higher. That combination should not produce a bank rally under the standard model – lower rates mean cheaper deposits, wider spreads, more lending. The standard model is missing something.

The KRE tracks the S&P Regional Banks Select Industry index. It holds 147 banks with an average market cap of $7.7 billion. Price to book sits at 1.26 times. Earnings yield runs around 8.6%. Top holdings include Popular Inc, East West Bancorp, Zions Bancorp, Valley National Bancorp, UMB Financial, Western Alliance Bancorp, Bank OZK, Flagstar Bank, Associated Banc Corp, and Wintrust Financial Corp.

The ETF ran up 13.6% to start the year, then went nowhere from Feb. 5 to June 1. That flat period coincided with the Iran war scare and a wave of private credit distress headlines. On June 3, Partners Group capped redemptions on its $8.6 billion Global Value SICAV evergreen fund after withdrawal requests hit roughly 10% of NAV. Shares plunged 17%. The next day, Partners Group warned it could cap withdrawals across more funds. Blackstone, KKR, and Ares fell in sympathy.

Yet the KRE finished higher on the June CPI report, a print that showed higher inflation at the producer and supplier level. That is not the kind of data that normally lifts rate-sensitive stocks.

The disconnect comes down to a mechanical shift in how banks earn money. The old model – borrow short, lend long – was broken during the deep yield curve inversion of 2022-2023. Long-term rates minus short-term rates hit minus 93 basis points in July 2023. That spread is now plus 49 basis points. The curve is no longer inverted. The market is not demanding a steep curve. It just needs the inversion gone.

A regional bank's earning assets sit in two buckets. The securities portfolio is the underwater bond book. Banks added nearly $2.3 trillion in securities from the start of 2020 to the end of 2021, when rates were near zero. Those bonds are mostly residential mortgage-backed securities and Treasuries, classified as held-to-maturity so unrealized losses do not hit earnings. As of Q4 2025, the FDIC's quarterly banking profile showed those losses are still large. Bonds mature. Each quarter, some slice of that portfolio rolls off. The bank takes the cash and either reinvests at higher yields or pays down expensive borrowings.

Commerce Bancshares described roughly $300 million in bonds rolling off at an average yield around 2.98%, being reinvested in the mid-to-high threes. That is 70 to 100 basis points of incremental yield on every dollar that reprices. Many banks are choosing not to reinvest at all, letting the bond book shrink and redirecting cash into higher-yielding loans or paying off FHLB borrowings.

The loan book is the bigger story. A typical regional bank's loan portfolio contains a mix of adjustable-rate loans – commercial and industrial lines, CRE floating-rate – and fixed-rate loans originated during 2020-2022. At Prosperity Bancshares, 36% of the loan book was fixed-rate as of September 2025. That ratio varies by bank. The point is the same: a huge slug of loans made at 3-4% are now coming due.

Consider a fixed-rate CRE loan originated in 2021 at 3.5%. It matures in 2026. The bank can now originate a new loan at 6-7%. That is a 300 to 400 basis point pickup on the same dollar of assets, going straight to net interest income. It is not a one-time event. It is a rolling wave. Every quarter, another tranche of 2020, 2021, and 2022 vintage loans hits its maturity date and resets higher.

Regions Financial reported that new production fixed-rate asset yields continue to benefit from elevated long-term interest rates. The bank added $4.5 billion of forward-starting hedges beginning throughout 2026 to lock in a portion of expected future loan and securities rate levels. That is a bank confident enough in the repricing tailwind to use derivatives to lock in the benefit.

The math is straightforward. Take a hypothetical regional bank with $20 billion in total earning assets. Roughly 15-20% of the combined portfolio reprices each year through maturities, amortization, prepayments, and floating-rate resets. That is $3-4 billion annually. If the repricing delta is 200 basis points on average – old yield of 3.5% replaced with new yield of 5.5% – that is $70 million in incremental annual net interest income. For a bank with total NII of $600-700 million, repricing alone adds roughly 10% to NII each year. A 25-basis-point Fed move would affect NII by maybe $10-15 million. The repricing engine is four to five times more powerful than any single rate move.

First Bancorp's net interest margin expanded 38 basis points year-over-year. The yield on earning assets rose 5 basis points. The cost of total liabilities fell 38 basis points. That margin expansion came almost entirely from the rolling repricing of old fixed-rate assets plus disciplined deposit cost management, not from any Fed action.

The reason this tailwind is durable is that fixed-rate assets originated in 2020-2022 have staggered maturities. Three-year loans and short Treasuries have already repriced. Five-year stuff is repricing now, which is why Q1 2026 earnings showed strong NIM expansion. Seven-year and ten-year loans are still to come. Long-duration MBS will trickle in for years.

Futures markets are pricing fed funds near 3.8% by late 2026 and around 4% by mid-2027. That is only 5 to 30 basis points above current levels. The market is not pricing a return to 5.5%. It is pricing rates staying roughly here, possibly drifting slightly higher. That is a world where banks earn more on new loans, not less.

There is a second catalyst. The Federal Reserve, FDIC, and OCC jointly proposed overhauling U.S. bank capital rules in March 2026. The proposal replaces the 2023 Basel III Endgame framework with a reduced-stringency version estimated to provide $87.7 billion in system-wide CET1 relief. Large regional banks would see reductions of roughly 5.2%. Smaller banking organizations would see 7.8%. The package lowers capital requirements overall, reduces duplication, and improves the economics of traditional lending. Deregulation could allow banks to hold less capital against loans and hold riskier, non-investment-grade loans on their balance sheets. Lower capital requirements mean more lending, more buybacks, higher ROE. For a sector trading at 11 to 13 times earnings, that is a powerful re-rating catalyst.

The KRE relative to the XLF – large banks – shows that small banks have underperformed since October 2022. Lately that ratio has shown some strength. The question is whether balance is being restored.

The real estate ETFs tell a similar story. The State Street Real Estate Sector ETF and the Vanguard Real Estate ETF have not done well. Both are supposed to be interest rate sensitive. In an environment with fewer rate cuts and potential hikes, either the market is not pricing in the risk or it is shrugging it off.

The broader point is that the model many investors use to think about banks is incomplete. A rising rate environment can still be profitable. The rate of change matters more than the level. The 2022-2023 period was destructive because rates rose rapidly. The 2025-2026 period is profitable because rates are elevated but stable. The repricing wave is mechanical, predictable, and multi-year. It does not need the Fed to do anything. It just needs time to roll through the balance sheet.

For a retail investor with a multi-year time horizon, the question is whether to be bothered by the quarterly noise of rate expectations, CPI prints, and private credit scares. The data suggests the underlying mechanics are working in favor of the banks regardless of what the next Fed meeting produces.