The fastest-growing AI companies are ditching the customer success playbooks that dominated B2B for a decade. At the FDE/CS Summit during SaaStr AI Annual 2026, leaders from Assembly AI, Lovable, and Harvey detailed what they threw out and what replaced it. For investors, the shift is not a back-office tweak. It is a direct signal of how these companies protect revenue, reduce churn, and scale without bloat.

Four hours of conversation produced a clear pattern. The market is moving from usage-based retention to outcome-based retention, and the companies that engineer that transition earliest will command higher multiples. Here is what changed and what it means for anyone tracking private AI valuations or the public SaaS benchmarks they will eventually face.

Assembly AI Rebranded Its CS Role to Fix Pipeline

Ryan Seams, who leads customer success at Assembly AI, conducted a listening tour and watched technical buyers physically recoil at the title “head of customer success.” To a developer, that title signals a commercially minded message-relayer who runs the QBR and pushes renewal. Assembly tried renaming the role to technical account manager, and recruiting collapsed – two good candidates in two and a half months.

The fix: forward deployed engineer. The job description barely changed. The brand did. Pipeline filled with the right people almost immediately.

Practical rule: Audit what your customer-facing titles signal to technical buyers. The word on a Slack profile determines whether a customer leans in or shuts down before the first sentence. For investors, this matters because poor title-market fit wastes months of sales cycle time that shows up as slow net-new logo acquisition and weak expansion.

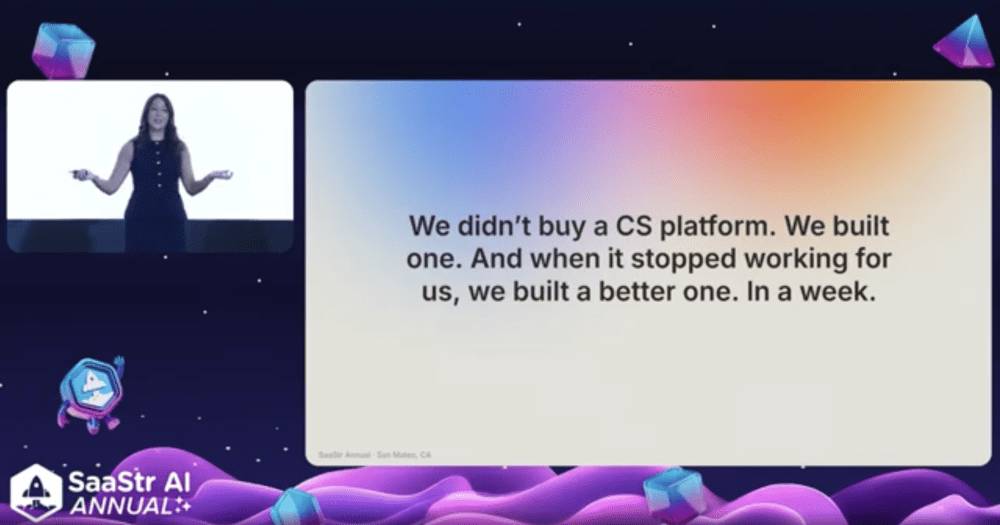

Lovable Dropped “AI” From Customer Conversations

Monica Perez runs customer success at Lovable, the fastest company in the world to reach $400M. Her most contrarian move: stop talking about AI as the headline. Every deck in the room said “AI-powered,” and her argument is that leading with it signals you are not thinking ten steps ahead. AI is becoming the baseline, the water the fish swims in, not the story.

Lovable’s onboarding does not open with what AI can do. It opens with what the customer will unlock. Perez replaced Gainsight with a command center built inside Lovable itself – tracking portfolio risk in real time, surfacing expansion signals, and generating individualized living hubs for every customer. When the tool stops working, the team versions it weekly. Her reasoning: the team closest to the customer should own the tool, and waiting for a vendor’s 12-month roadmap is now the constraint, not the engineering budget.

Key insight: The build cost for internal CS infrastructure has collapsed. Companies that treat rigid third-party platforms as the bottleneck are losing weeks per quarter. Investors should watch whether a company builds its own CS stack or remains dependent on legacy vendors – the former signals speed and alignment, the latter signals inertia.

Harvey’s High-Touch Approach Is a Moat, Not a Relic

Tom Ronen, VP of customer success at Harvey, made a confession that cut against the AI-native narrative. Harvey runs an old-school motion: executive business reviews, heavy on-site work, change management frameworks that look like they were printed by a Big Four consultant two decades ago. At an $11B company crossing $190M ARR with 100,000+ attorneys across 60+ countries, that is the deliberate choice.

Selling AI into a 200-person law firm is not selling software. It is selling a fundamental change in how partners who have practiced the same way for 30 years do their work. No automated QBR or health score gets you there. Harvey tracks five ROI pillars and asks CSMs to tag value stories against them, because the goal is reducing non-billable work and speeding up matters, not racking up active users.

Risk to watch: If the company’s health score still leans on login frequency, it is measuring the wrong thing in an AI product. Harvey’s approach proves that high-touch is a moat when the sale requires deep behavior change inside a skeptical organization. Investors in vertical AI plays should demand to see outcome-based metrics, not usage metrics, before assigning a premium.

The Change Management Multiplier

Ronen cited a Harvard study of 1,515 startups. Both groups got the same AI tools and the same training. One group additionally received a single document describing how teams like theirs had used the tools successfully. That one piece of change management produced 2x more revenue and made the group 18% more likely to acquire paying customers. A Microsoft survey of 500 enterprise decision-makers landed in the same place: AI vision and change-management confidence correlated with success above the technical factors.

What this means: Change management is not the soft, unmeasurable part of the sale. It is one of the highest-return inputs to revenue, and a small, deliberate investment compounds. For investors, the question is whether the company has built change management into its CS motion or is leaving it to chance.

The Unit of Work Framework Predicts Revenue

John Gleeson, who took Motive’s CS from $1M to over $300M ARR and now runs the applied-AI fund SuccessVP, gave the sharpest framework of the day. AI succeeds when two conditions are met: high context and verifiable correctness. Code has both baked in, which is why every company hitting $100M ARR in under a year is a developer tool – Cursor in 12 months, Bolt in 14, Lovable in 8, Replit’s agent from $10M to $100M in six. Most domains do not get those conditions for free. Somebody has to engineer them, and that somebody is now the vendor’s CS team.

Put the two conditions together and you get a unit of work, and the unit of work is the unit of revenue. Investors can use this framework to separate winning AI plays from hype: if the vendor cannot name the discrete outcome a customer pays for, the business model is fragile.

NPS Is Dead for Revenue Forecasting

A panel with Bobby Cooper (Retention Intelligence), Ashvin Vaidyanathan (LinkedIn), Daniel Silverstein (Carta), and Ursula Llabres (Content Square) reached a rare consensus: kill NPS. Response rates are low, and the people not responding are often the ones churning. The survey catches customers at an arbitrary moment in time, and there is no clean correlation to gross revenue retention. Llabres named the tell directly: a great NPS score sitting right next to weak retention. They are loving you in the survey and leaving with their wallets.

Silverstein cannot fully kill it because the board still asks, so he supplements with CSAT and CES and aggregates rather than trusting one number.

Bottom line for traders: If a public SaaS company still uses NPS as a leading indicator in its investor materials, push for transaction-level signals and product telemetry that actually correlate with renewal. The private companies moving fastest have already abandoned it.

Closing the Win Line Fixes Churn

Cooper described a shift Weave made on its way from $8M to $200M ARR through IPO. They stopped letting sales or RevOps mark a deal closed-won at signature. A deal only counted as booked once the customer crossed a defined success threshold inside implementation. That single change fixed the handoff problem – a signed deal that never kicked off was never counted – drove sales to qualify harder for customers likely to succeed, and took churn from 4% per month down to roughly half a percent while scaling.

Practical rule for investors: Look at where the company draws the closed-won line. Pulling it into implementation, tied to a real activation milestone, aligns sales and CS around the same outcome and surfaces failure-to-launch churn before it compounds.

The Investor Takeaway Across All Five Signals

The customer success function is no longer a cost center that protects renewal. In the fastest AI companies, CS is the mechanism that proves value, reduces time-to-first-outcome, and compounds revenue through change management. Companies like Lovable, Harvey, and Assembly AI are rewriting the playbook in real time, and the numbers – 2x revenue lift from one document, churn dropping from 4% to sub-1%, pipeline filling after a title change – confirm the leverage.

For investors, the next step is simple: before adding a position in any private or public AI company, ask which of these five shifts the company has made. The absence of any of them is a red flag. The presence of all five is a compounding advantage that the market has not priced in.