Back to Markets

Macro● Neutral

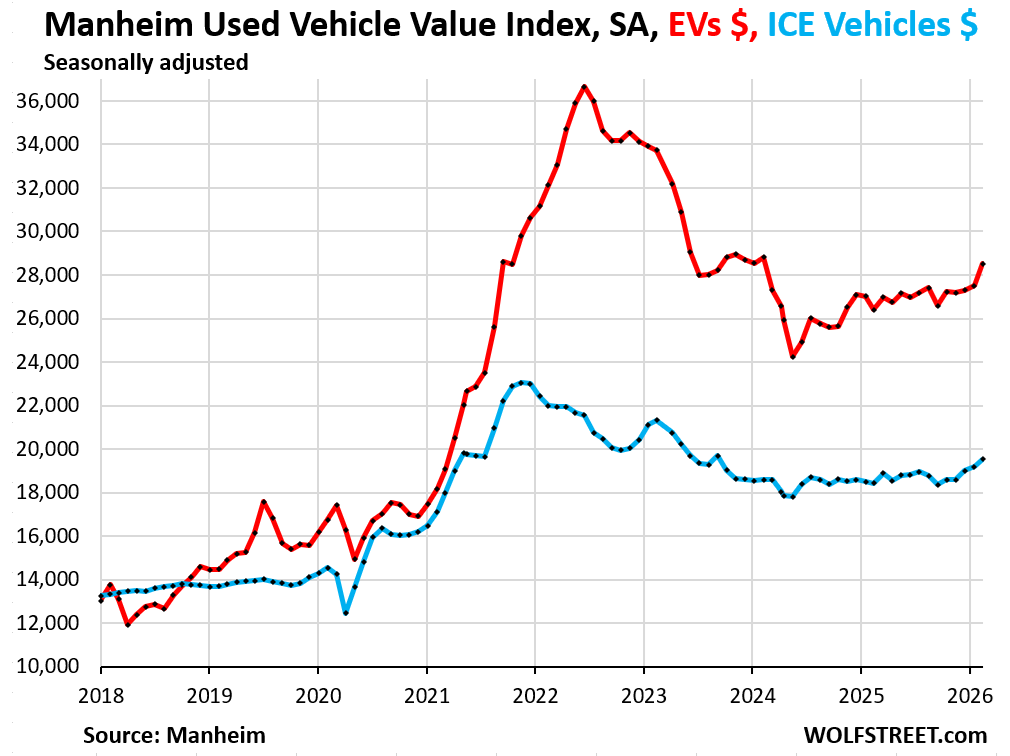

Used Vehicle Price Surge Risks Renewed Inflationary Cycle

Wholesale automotive costs are rising again, threatening to derail disinflation. Expect retail price impacts within 60 days as Fed rate policy tightens.

Continue with

A Sudden Reversal in the Wholesale Market

For market participants monitoring the long-tail effects of post-pandemic inflation, the latest data from the wholesale automotive sector provides a sobering reminder of how quickly price pressures can re-emerge. Used vehicle prices, which had finally begun to show signs of stabilizing, have experienced a sudden and sharp upward trajectory. This shift is occurring at auctions where dealers replenish their inventories, a critical pipeline that historically acts as a leading indicator for consumer-facing inflation metrics.

This recent uptick is drawing uncomfortable parallels to the early months of 2020, a period that preceded a historic, multi-year surge in broad-based inflation. For traders and macro analysts, the question is no longer just about the current price action, but whether this represents a transient anomaly or the beginning of a persistent, sticky inflationary trend that could complicate central bank policy trajectories.

The Mechanism of Price Transmission

When wholesale used vehicle prices climb, the transmission to the retail market is almost mechanical. Dealers facing higher acquisition costs at auction must pass those expenses along to consumers on the lot. Because used vehicle prices are a significant component of the Consumer Price Index (CPI), this volatility has a disproportionate impact on the headline inflation numbers that the Federal Reserve scrutinizes when setting interest rate policy.

In 2020, the supply chain bottlenecks and inventory shortages in the automotive sector were among the first signals that the transitory narrative was losing ground. The current spike suggests that supply-demand imbalances in the automotive space are far from resolved. Dealers are finding it increasingly difficult to source quality inventory, and the competition for available units is driving prices back toward levels that many analysts assumed were firmly in the rearview mirror.