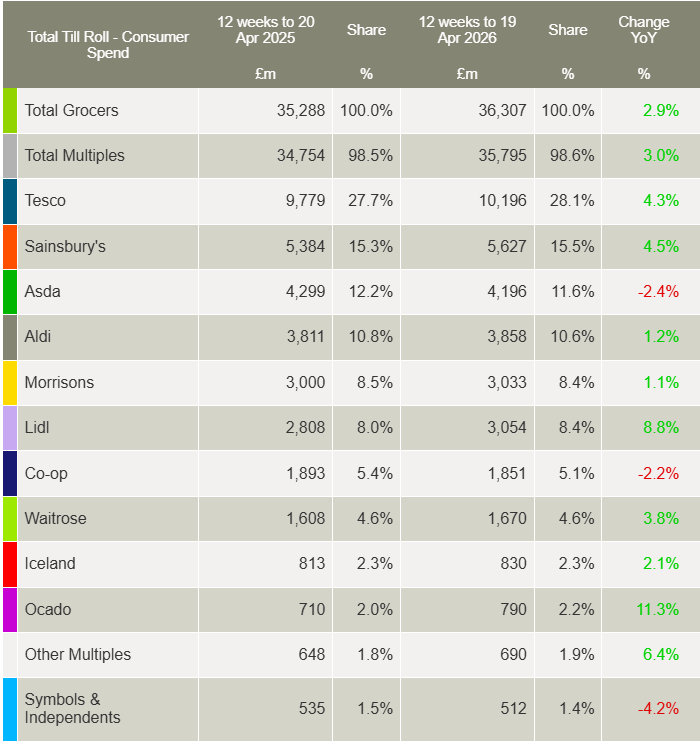

British grocery spending growth slowed to 0.9% in the four weeks ending April 19, 2026, signaling a shift in household behavior as external geopolitical pressures weigh on domestic consumption. This marginal increase reflects a broader trend of shoppers prioritizing value and discount-focused purchasing strategies. The data suggests that inflationary pressures, combined with heightened uncertainty regarding supply chains linked to Middle East instability, are forcing a recalibration of household budgets.

Shifting Patterns in Consumer Spending

Retailers are observing a distinct move toward defensive spending habits. As shoppers navigate a period of constrained disposable income, the preference for private-label goods and promotional offers has intensified. This behavior is a direct response to the volatility in global logistics, which continues to influence the cost of imported goods and the availability of specific product categories. The modest growth rate indicates that while volume demand remains relatively stable, the total value of the basket is being suppressed by a collective effort to mitigate rising costs.

Supply Chain Sensitivity and Retail Margins

The retail sector is currently navigating a complex environment where operational costs are increasingly tied to geopolitical developments. Disruptions in major shipping lanes have created a ripple effect, forcing supermarkets to manage inventory more aggressively to avoid stockouts while maintaining competitive pricing. For investors, the concern lies in whether retailers can sustain their current margins if the trend of value-seeking behavior persists alongside elevated logistics expenses.

This environment places significant pressure on stock market analysis regarding the resilience of consumer staples. While grocery retailers typically benefit from inelastic demand, the current shift toward lower-margin, value-tier products may compress earnings growth in the coming quarters. The reliance on promotional activity to drive foot traffic is a clear indicator that the consumer is no longer willing to absorb price hikes without a corresponding value proposition.

AlphaScala Data Context

AlphaScala tracking shows that the current 0.9% growth rate in grocery spending is significantly below the trailing twelve-month average for the sector. This deceleration suggests that the initial phase of post-inflationary recovery has stalled, leaving retailers with limited room to maneuver on pricing strategies.

The Next Marker for Retail Performance

The next critical indicator for the sector will be the upcoming quarterly earnings reports from major UK supermarket chains. These filings will provide the first concrete look at how management teams are balancing promotional costs against the need to protect operating margins. Investors should look for specific commentary on inventory turnover rates and the impact of sustained logistics surcharges on net income. The ability of these firms to maintain market share without eroding profitability through excessive discounting will determine the sector's trajectory through the remainder of the year.