The narrative that geopolitical cooling in the Middle East will trigger a return to low-cost crude ignores the fundamental shift in production economics within the United States. While regional tensions often dictate short-term volatility, the long-term price floor for oil is increasingly determined by the capital discipline and operational efficiency of domestic shale producers. Companies like Diamondback Energy have moved away from aggressive growth models, focusing instead on maintaining low breakeven points that insulate their balance sheets from price swings.

Operational Efficiency and Breakeven Resilience

The shift toward capital efficiency in the Permian Basin has fundamentally altered how producers respond to global supply fluctuations. Rather than reacting to every headline with a surge in drilling activity, firms are prioritizing free cash flow and shareholder returns. This disciplined approach means that supply is no longer as elastic as it was during the shale boom years. When global supply chains face disruption, the lack of rapid, low-cost production expansion in the U.S. prevents the rapid inventory builds that previously suppressed prices.

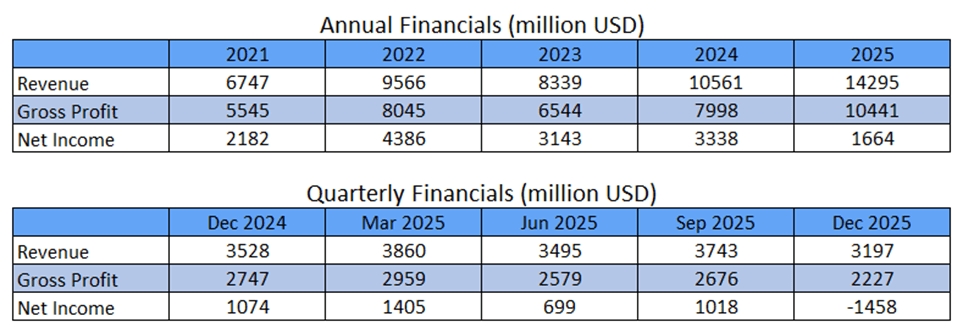

Diamondback Energy exemplifies this trend through its focus on scale and cost control. By maintaining a lean cost structure, the company ensures that its operations remain profitable even if global benchmarks experience downward pressure. This operational posture provides a buffer that is increasingly rare in the energy sector, making the stock a focal point for those looking at energy exposure through the lens of structural, rather than cyclical, value. Current AlphaScala data for FANG stock page reflects this, with an Alpha Score of 54/100 and a Mixed label, highlighting the balance between its strong production profile and broader energy sector volatility.

Inventory Dynamics and Global Supply Constraints

Global oil inventories remain sensitive to refining throughput and geopolitical bottlenecks. Recent data suggests that even when crude supplies appear adequate, refining constraints can create localized shortages that keep the price of end-market products high. This disconnect between crude availability and refined product output is a primary driver of sustained energy prices. As detailed in U.S. Crude Inventories Build Unexpectedly as Refining Throughput Stalls, the inability of the refining sector to consistently process crude into usable fuel prevents the market from fully normalizing.

Producers are now operating in an environment where the following factors dictate the next move for the sector:

- Capital allocation strategies that prioritize debt reduction over new well development.

- Refining capacity utilization rates that remain sensitive to maintenance schedules and operational bottlenecks.

- The persistent gap between global demand growth and the slow pace of new upstream investment.

Investors should monitor the upcoming quarterly production guidance and capital expenditure updates from major Permian operators. These filings will provide the next concrete marker for whether the industry intends to maintain its current discipline or if shifting price environments will tempt a return to production expansion. For those tracking broader commodity trends, further commodities analysis remains essential to understanding how these domestic production realities interact with global market pressures.