Back to Markets

Macro● Neutral

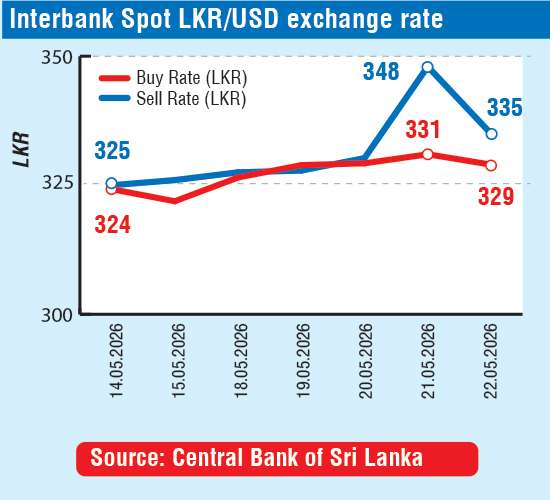

Sri Lanka Rupee Finds Floor as CBSL Imposes Rs. 330 Cap

Sri Lanka rupee stabilized at 329/335 after CBSL capped interbank spot at 330. The cap halts panic demand, risks a two-tier market if reserves fall short.

Continue with

The Sri Lankan rupee ended its two-day slide on Friday after the Central Bank of Sri Lanka (CBSL) forced a cap on the interbank spot rate. Commercial banks were instructed to quote a maximum bid of Rs. 330 per dollar. The market settled around Rs. 329/335, compressing sharply from Thursday's disorderly range of Rs. 331/348.

The previous session had seen panic dollar demand from importers and delayed exporter conversions widen the bid-ask spread. The CBSL's directive removed the uncertainty premium that had driven the extreme volatility. A simple reading is that the central bank restored order with a single administrative tool. The better market read is more cautious. A hard ceiling does not eliminate the underlying demand-supply imbalance. It shifts it.

Exporters who delayed conversions may now accelerate repatriation to capture the capped rate. That provides temporary relief. Importers and energy companies with open dollar needs face a narrower window to cover. They risk a build-up of deferred demand that could test the cap if the CBSL does not supply enough dollars from reserves concurrently.

Import Costs and Bond Yields in the Path

The cap's immediate effect is on pricing in the real economy. Fuel, pharmaceutical, and food importers now transact at a tighter rate. That should slow pass-through to retail prices in the coming weeks. It is a net positive for inflation expectations and the CBSL's monetary policy credibility.