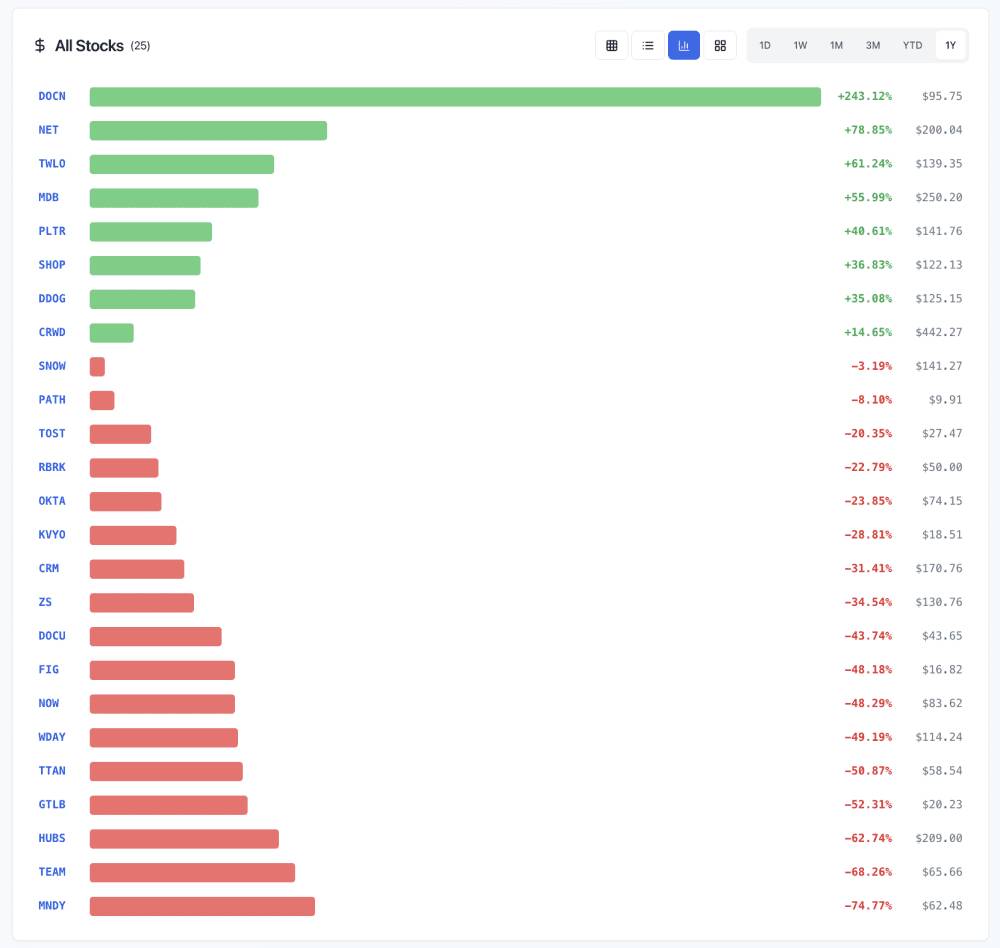

The software sector experienced a sharp contraction this week as a wave of selling pressure hit major enterprise technology providers. The sudden decline, characterized by double-digit percentage drops at the open for industry bellwethers, suggests a rapid repricing of growth expectations across the broader software landscape. While the immediate reaction was severe, the divergence between weekly volatility and the broader 12-month performance trajectory remains a critical point of focus for institutional capital allocation.

Sector-Wide Contagion and Enterprise Demand

The sell-off originated with specific earnings-related disappointments that triggered a broader reassessment of enterprise software spending. ServiceNow, IBM, Salesforce, and Oracle all faced significant downward pressure as investors reacted to shifts in guidance and perceived demand saturation. The contagion effect moved quickly through the sector, impacting firms like Intuit and others that rely on consistent subscription-based revenue models. This movement highlights a potential pivot in how the market views the durability of cloud-based recurring revenue in an environment where capital expenditure efficiency is increasingly prioritized over top-line growth.

AlphaScala data currently reflects a cautious outlook for legacy and cloud-integrated firms, with IBM stock page holding an Alpha Score of 40/100, while CRM stock page and ORCL stock page each sit at 38/100, all labeled as Mixed. These scores underscore the current difficulty in distinguishing between temporary market turbulence and a fundamental shift in the software business cycle.

Valuation Realignments and Future Growth Paths

The sharp decline in equity value forces a conversation regarding the valuation multiples assigned to software companies. For much of the past year, the sector benefited from a narrative of resilient enterprise demand and artificial intelligence integration. The current volatility suggests that the market is no longer willing to pay a premium for growth that does not translate into immediate margin expansion or clear operational efficiency gains.

Investors are now looking for specific indicators to determine if this correction is a healthy reset or the beginning of a sustained downturn:

- The ability of firms to maintain subscription renewal rates despite tightening corporate budgets.

- The conversion rate of AI-related pilot programs into long-term, high-margin enterprise contracts.

- The impact of increased competition on pricing power within the cloud infrastructure and CRM segments.

The next concrete marker for this sector will be the upcoming round of mid-quarter guidance updates and subsequent 10-Q filings. These documents will provide the necessary transparency to determine if the recent price action was driven by a temporary liquidity event or a fundamental deterioration in the underlying software business models. As the market digests these moves, the focus will shift toward whether the current valuation levels provide a sufficient margin of safety for long-term holders or if further downside remains as firms adjust to a more disciplined spending environment.