Back to Markets

Macro● Neutral

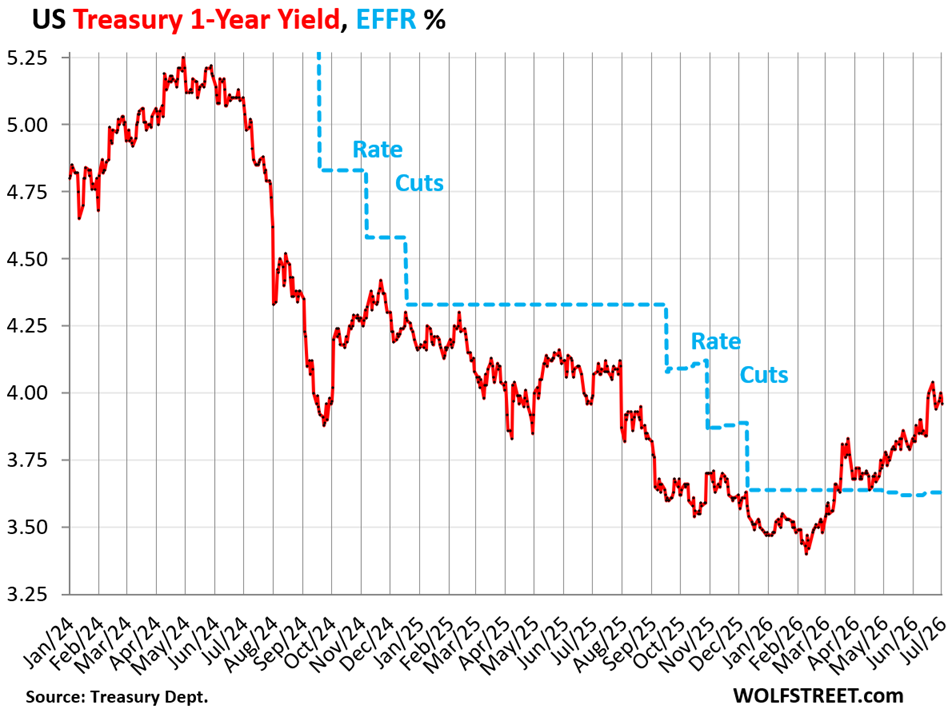

Six-Month Yield at 4%: Bond Market Tells Fed to Hike

The six-month Treasury yield surged 50bps since January, now 35bps above the Fed's policy rate. Banks raise CD yields above 4%. Next week's 1-year T-bill auction will test whether the market expects a hike before year-end.

Continue with

The government sold $84 billion of six-month Treasury bills this week at an investment rate of 3.97%, up 17 basis points from the auction two weeks ago. In the secondary market, the six-month yield touched 4.0% earlier in the week before closing at 3.97% on Thursday, according to Treasury Department data.

Since early January, the six-month yield has surged nearly 50 basis points. It now sits 35 basis points above the effective federal funds rate, a reversal from January when it traded below the policy rate. The yield gap indicates the bond market expects at least one rate hike within the next six months, possibly more.

The three-month yield tells a similar story. It closed at 3.82%, 19 basis points above the EFFR, after pushing as high as 24 basis points above earlier in the week. Even inside a three-month window, the market sees a reasonable chance of a rate increase.

The one-year yield has been near or above 4.0% for the past two weeks, up about 60 basis points from early February. Over five months, the one-year yield flipped from pricing rate cuts to pricing rate hikes.

Six-Month Yield at 4%

Banks have responded by raising yields on brokered CDs sold through stock brokers. Many CD yields have moved above 4% to compete with T-bills for retail cash.

Fed Chair Kevin Warsh has been telling the bond market to watch the data, not the Fed. The Fed wants the bond market as a clean data input, he said. If the market reacts to what it thinks the Fed will do instead of what the data says, that input gets polluted. The market is watching the data. It sees a jobs market that has not softened and inflation that has not receded to target. At the June 17 FOMC meeting, 9 of the 19 members projected at least one rate hike this year. Warsh did not disclose his own projection. Resistance to hiking at the Fed is fading.