Sabine Royalty Trust (NYSE:SBR) declared a May distribution of $0.4979 per unit, good for a 6.2% annualized yield. The payout reflects oil production from February 2026 and gas production from January 2026 – meaning the current oil price spike tied to the Iran conflict has not yet shown up in the trust's cash flows.

The trust produced 56,677 barrels of oil at $60.97 a barrel during the period, up from 44,645 barrels at $57.57 in the prior month. Gas output hit 1.20 million cubic feet at $3.98 per Mcf, versus 885,409 Mcf at $3.42. The 27% jump in oil volumes drove the distribution higher than April's $0.32497 per unit.

SBR is a royalty trust, not an operator. It holds mineral interests in producing wells across Florida, Louisiana, Mississippi, New Mexico, Oklahoma and Texas. The trust has no drilling costs, no capital budget, and no exploration risk. Royalty income flows through to unitholders with virtually no expense drag. That structure means the trust's lifespan depends entirely on reserve depletion, not on management decisions.

When Sabine Corporation formed the trust in 1982, estimated reserves stood at 9 million barrels of oil and 62 billion cubic feet of gas. The trust was expected to deplete by 1993. Instead, it has produced more than 25 million barrels and 79.6 billion cubic feet over 44 years. Current reserve estimates show 9.3 million barrels of oil and 60.7 billion cubic feet of gas remaining, suggesting another 8 to 10 years of payouts at current production rates.

Year to date, SBR has distributed $1.71 per unit. Over the same five-month stretch in 2025, the trust paid $2.13. The decline reflects lower realized prices in the production months that feed the early-2026 distributions. As higher oil prices from the Iran conflict roll into future production months, the payout trajectory should improve.

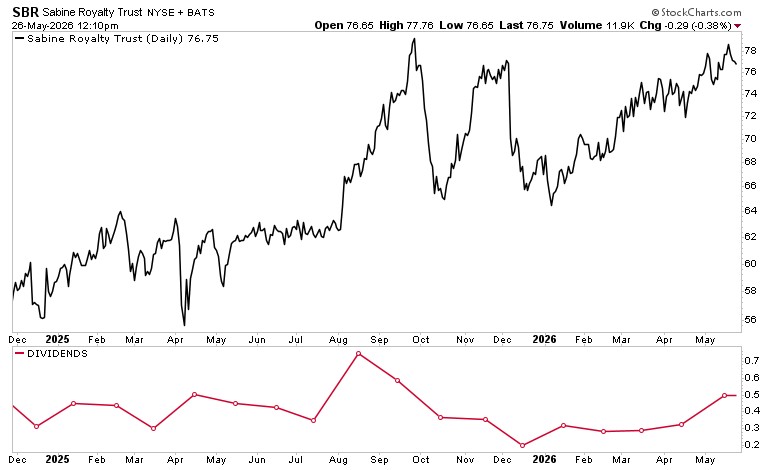

SBR units trade at $76.75, up 14.6% year to date and 24% over the past 12 months. The record high of $91.10 came in January 2023. Institutional holders have increased to 166 from 129 a year ago, according to Yahoo Finance data. Major holders include Americana Partners, Morgan Stanley and Beacon Pointe Advisors.

The trust has not missed a monthly distribution since 2005. That track record reflects the pass-through structure: as long as the wells produce, the cash flows reach unitholders. The current yield of 6.2% sits well above the S&P 500 dividend yield, though the trust's unit price carries commodity price risk and depletion risk that a broad index does not.

For investors comparing SBR to other energy income vehicles, the key distinction is the absence of operating leverage. A driller's cash flow gets squeezed between oil prices and rising service costs. SBR's cash flow is simply price times volume, minus trust expenses. That makes it a direct play on oil and gas prices, with no management execution risk.

The next distribution will reflect March oil production and February gas production – the first period that includes post-Iran-conflict pricing. If realized prices track the crude oil and natural gas benchmarks from those months, the payout should increase further.