Back to Markets

Indices● Neutral

RYLD Strategy Faces Limits as Russell 2000 Volatility Shifts

The fund's 12% yield faces structural hurdles as small-cap swings threaten upside participation. Watch upcoming option cycles for potential yield compression.

Continue with

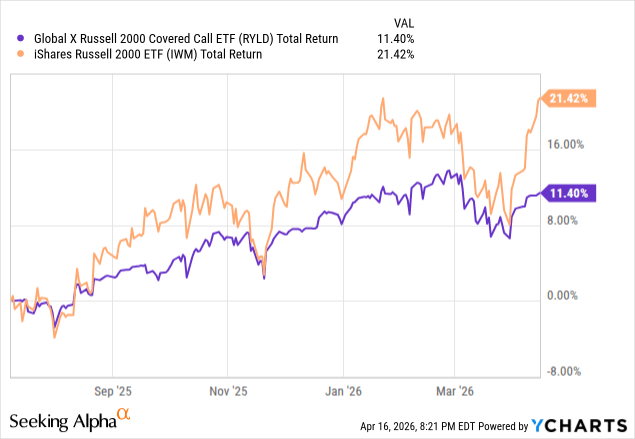

The Global X Russell 2000 Covered Call ETF (RYLD) has entered a period of structural testing as the underlying small-cap index struggles to find a consistent directional trend. By selling at-the-money call options on the Russell 2000, the fund effectively caps its participation in market rallies while collecting premiums that generate a double-digit yield. This mechanism functions optimally in sideways markets, but recent index behavior has highlighted the limitations of a strategy that sacrifices upside potential for immediate cash flow.

Structural Constraints of Covered Call Income

The core value proposition of RYLD rests on the volatility of the Russell 2000. When the index remains range-bound, the premiums collected from the covered call strategy provide a consistent income stream that often outperforms the price appreciation of the index itself. However, the fund faces a recurring hurdle when the Russell 2000 experiences sharp, sudden moves. Because the calls are sold at-the-money, the fund is forced to cap its gains during recovery phases, leaving investors with the downside risk of the underlying assets without the benefit of full participation in the subsequent rebound.

This dynamic creates a specific performance profile that diverges from traditional equity indices. While the market analysis often focuses on growth-oriented tech stocks, RYLD serves as a proxy for investors prioritizing yield over capital preservation or aggressive growth. The fund effectively converts equity volatility into a fixed-income-like distribution, but this conversion is only efficient if the underlying index does not breach the strike prices set by the option writing strategy.