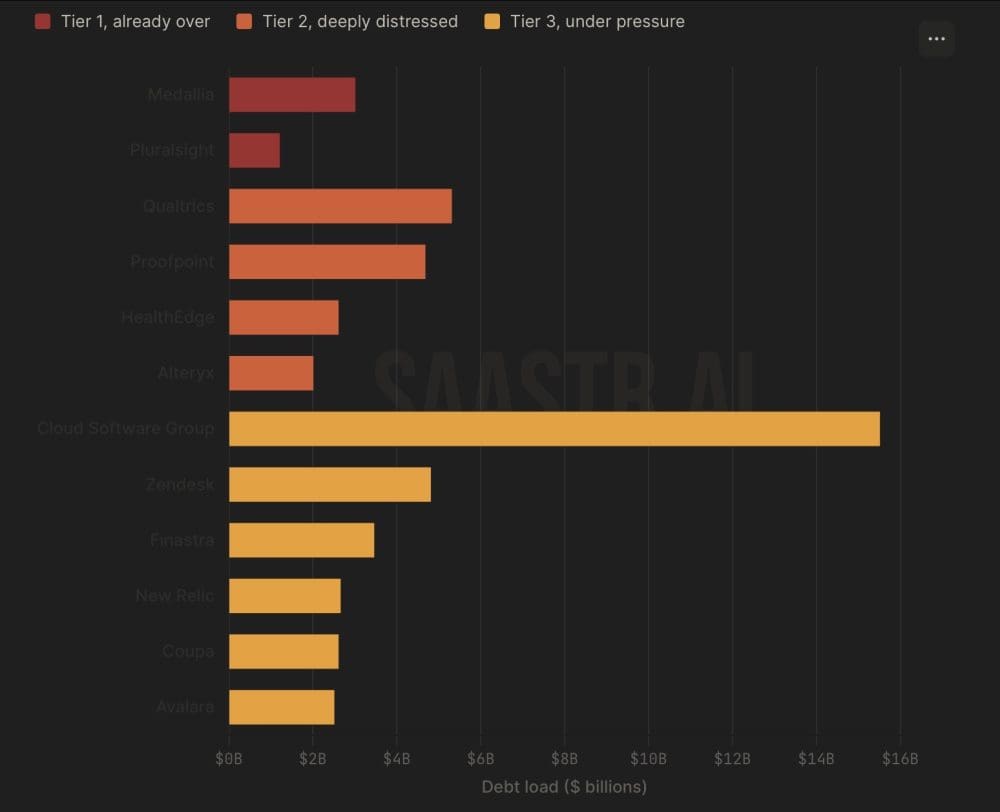

The transfer of Medallia from Thoma Bravo to a consortium of lenders marks a definitive shift in the private equity software landscape. By handing over control to creditors including Blackstone, KKR, Apollo, and Antares, the sponsor has effectively acknowledged that the 2021 acquisition valuation is no longer supported by the company's current capital structure. This transition wipes out the original equity stake, signaling that the high-leverage models utilized during the peak of the SaaS acquisition cycle are facing a severe reckoning.

Debt Servicing and the Valuation Gap

The Medallia restructuring highlights the friction between aggressive debt-funded growth strategies and the current interest rate environment. When private equity firms acquired software assets at high multiples, the underlying assumption relied on consistent revenue expansion and low-cost debt refinancing. As interest rates remained elevated, the cost of servicing these debt loads began to outpace the cash flow generation of the underlying businesses. This creates a structural bottleneck where the equity value is eroded by the necessity of prioritizing debt obligations.

This event serves as a bellwether for other software assets acquired during the same period. The risk is concentrated in firms that utilized significant leverage to bridge the gap between purchase price and operational earnings. As these deals approach maturity, lenders are increasingly forced to choose between extending terms or seizing control to protect their principal. The Medallia case demonstrates that lenders are no longer willing to wait for a market recovery that justifies the original entry multiples.

Sector Read-Through for Financial Sponsors

The involvement of major financial institutions in the Medallia restructuring suggests that the secondary market for distressed software assets is becoming more active. Major players are moving from a position of passive capital providers to active owners of operational software businesses. This shift forces a change in the management approach for these assets, moving away from growth-at-all-costs models toward a focus on immediate debt reduction and operational efficiency.

AlphaScala data currently reflects the complex environment for these financial institutions. KKR holds an Alpha Score of 47/100, labeled as Mixed, while BX maintains an Alpha Score of 52/100, also labeled as Mixed. These scores reflect the broader volatility within the financial sector as firms manage the fallout from legacy acquisition portfolios while navigating shifting credit markets. You can track further developments in the sector via the KKR stock page or the BX stock page.

Investors should monitor the upcoming maturity walls for similar software-focused private equity deals. The primary marker for the next phase of this trend will be the frequency of debt-for-equity swaps in the software space. If lenders continue to prioritize control over restructuring, the industry will likely see a wave of similar ownership changes. This process will ultimately reset the valuation floor for the entire SaaS sector, as the market adjusts to the reality that historical acquisition prices are no longer sustainable under current financing conditions. The next concrete indicator will be the disclosure of debt maturity profiles in upcoming quarterly filings for other major private equity-backed software platforms.