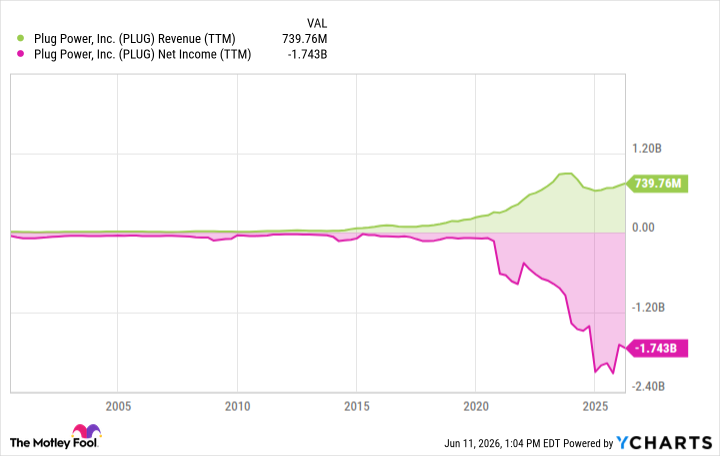

Plug Power has never turned an annual profit since going public. The company's accumulated deficit now sits at roughly $8.2 billion. Management is trying to change that with Project Quantum Leap, a plan to cut costs and lean into higher-margin businesses like electrolyzers.

In the first quarter, the strategy showed early signs of working. Plug Power reported a gross margin of negative 13%, a sharp improvement from negative 55% a year ago. Adjusted earnings per share narrowed to a loss of $0.08 from $0.17. Management said on the earnings call that it expects to reach positive EBITDA by the fourth quarter.

That target depends on two things: electrolyzer sales and cheaper hydrogen supply.

Project Quantum Leap: Margins Tighten as Costs Fall

The margin improvement came partly from scaling in-house hydrogen production. Plug Power built plants in Tennessee, Georgia, and Louisiana with combined capacity of about 40 tons of liquid hydrogen per day. Producing fuel internally reduces the cost per kilogram, which directly lifts gross margins.

The company also signed a deal with a major industrial gas company. Management said the agreement produced a "substantial reduction in the cost per kilogram" of purchased fuel. That third-party arrangement lets Plug Power serve customers in the western and northeastern United States without expensive transportation costs.

Electrolyzer Revenue Jumps 343% on Europe's RED III Mandates

Electrolyzer revenue surged 343% year over year to $40.8 million in Q1. The company already generated $52.3 million in electrolyzer revenue in 2025, driven by European demand. The European Union's RED III directive requires 4 to 6 gigawatts of electrolyzer capacity by 2030. Plug Power is positioning itself to capture a piece of that buildout. Electrolyzers carry higher margins than the company's legacy equipment business, meaning each sale improves the blended gross margin.

The $8.2 Billion Hole and the Third-Party Hydrogen Deal

Despite the improvements, Plug Power still burned cash last year, losing $1.6 billion. The accumulated deficit is deep. The ability to reach positive EBITDA by Q4 will determine whether the stock can hold. Missing that target would likely trigger another round of dilution or debt restructuring.

For investors watching the transformation, the key metrics are gross margin and the cost of hydrogen per kilogram. Electrolyzer revenue growth is the variable that determines whether margins can turn positive. The Q4 EBITDA target is the next major checkpoint. Plug Power's cash position will be tested if margins remain negative beyond that quarter.