Stocks● Neutral

Households Pile $5.2 Trillion Into Money Funds as Real Yields Turn Negative

Households added $89B to money market funds in Q1, pushing balances to $5.21T. With inflation at 4.2% and MMF yields at 3.5%, real returns are now negative 0.7%.

Continue with

Households added $89 billion to money market funds in the first quarter, pushing total balances to $5.21 trillion, even as inflation began to outpace the returns those funds generate. The Federal Reserve's quarterly Z1 Financial Accounts show the pile has roughly doubled since the central bank started raising rates in early 2022.

MMFs currently yield about 3.5%, down from over 5% before the rate cuts began last September. Treasury bills, the closest substitute, offer between 3.66% (four-week) and 3.91% (one-year) at this week's auctions. Inflation, measured by the Fed-preferred PCE price index, hit 3.5% in March and surged above 4% in April and May. At May's CPI reading, the real yield on MMFs stands at negative 0.7%.

The mechanics are straightforward. MMF yields come from the short-term instruments they hold minus fees. Three-month Treasuries pay 3.71%, six-month Treasuries 3.80%, and asset-backed commercial paper yields 3.75% to 3.85% for 30- and 90-day paper. The gap between these rates and the 3.5% investors actually receive is the fee skimmed by the fund provider. The Fed's overnight reverse repo facility, which pays near zero, has seen near-zero activity as a result.

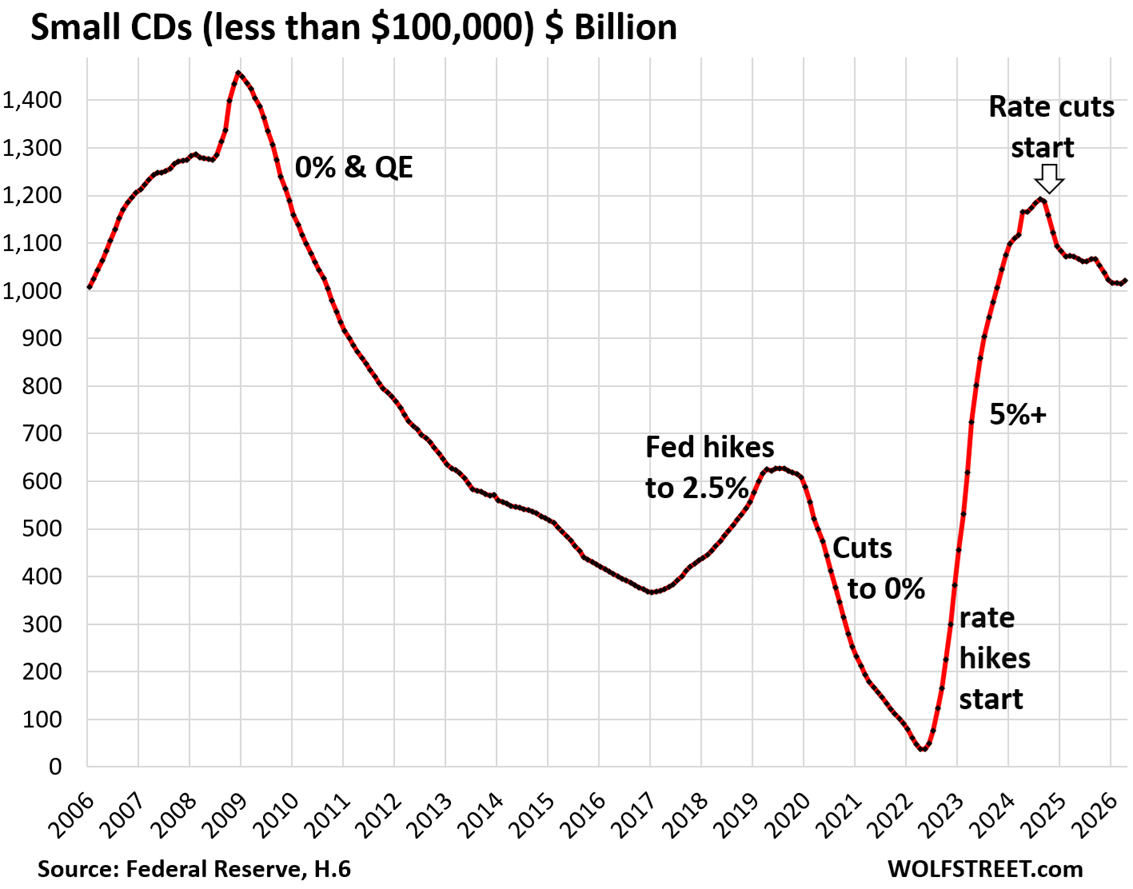

Banks are also seeing a flood of cash. Large time deposits – certificates of deposit of $100,000 or more – hit a record $2.52 trillion in April, up $49 billion from March and $169 billion year over year, per the Fed's H.8 report on bank balance sheets. Since rate hikes began in March 2022, large CD balances have surged $1.11 trillion. Small CDs, those under $100,000, ticked up to $1.02 trillion in April after six consecutive months of decline, the Fed's H.6 money stock data shows.