The Infrastructure Disconnect

For investors scanning the industrial sector for exposure to the artificial intelligence boom, the focus has largely remained on semiconductor manufacturers and hyperscale data center operators. However, a critical bottleneck has emerged that is arguably more important than the chips themselves: the power required to run them. GE Vernova (GEV), the energy-focused spin-off from the former General Electric conglomerate, is increasingly appearing structurally mispriced by the broader market, offering a compelling entry point for those betting on the long-term electrification of the global economy.

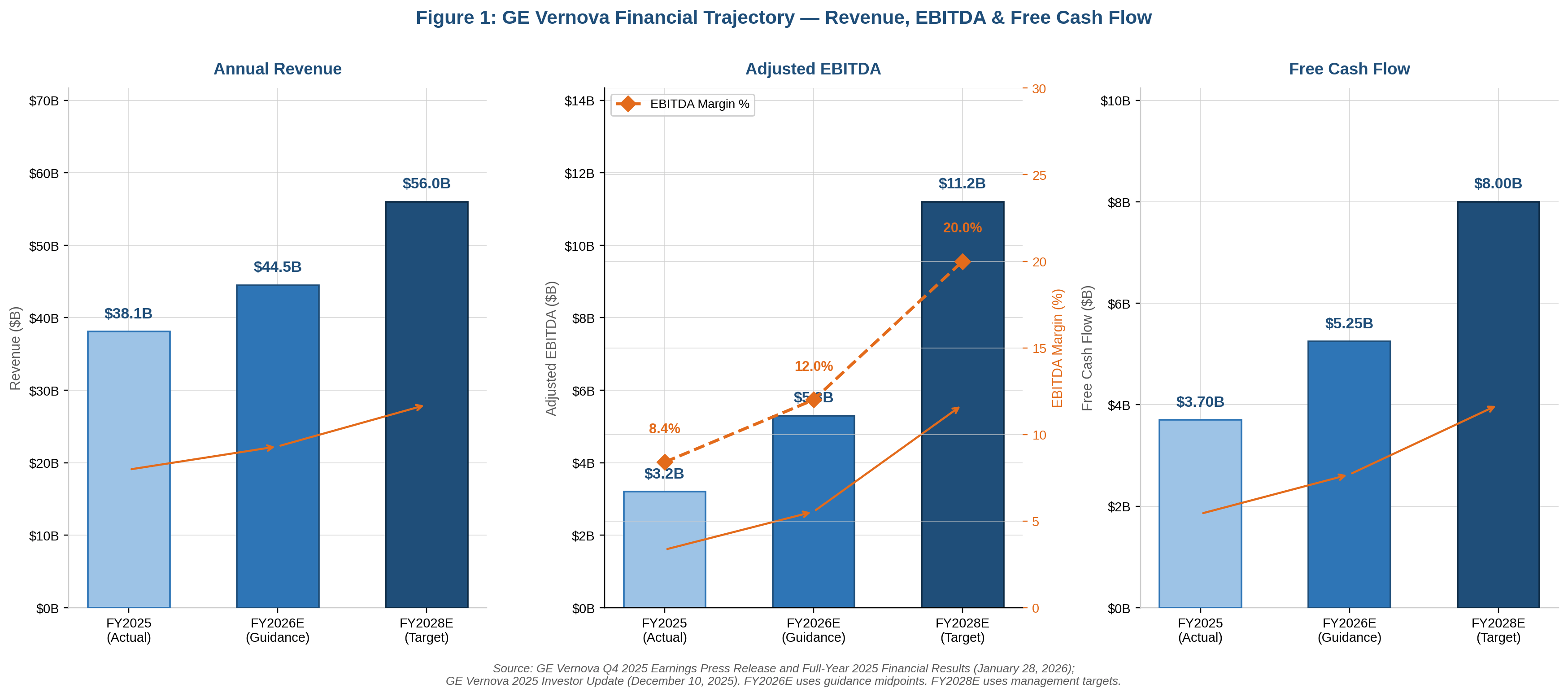

Despite a robust fundamental outlook, GEV’s current market valuation fails to account for the company’s massive $150 billion backlog. This figure is not merely a record of past successes; it represents a multi-year revenue runway that is increasingly composed of high-margin service contracts and long-term infrastructure commitments. As the global grid undergoes a massive modernization effort, GE Vernova stands at the nexus of the energy transition, positioning it as a primary beneficiary of the AI-driven power demand supercycle.

The Power Supercycle Thesis

The narrative surrounding GE Vernova is shifting from a standard industrial play to a critical utility-infrastructure provider. The unprecedented surge in data center construction has placed a strain on existing energy grids that few predicted even three years ago. With AI-driven compute power requiring significantly higher wattage per rack, the demand for reliable, baseload power—and the turbines to generate it—has reached an inflection point.

GE Vernova’s portfolio, which spans gas power, wind energy, and electrification, is uniquely suited to meet this demand. The company is currently executing on margin-accretive contracts that suggest a fundamental expansion in profitability. Unlike traditional manufacturing cycles that are sensitive to immediate consumer demand, GEV’s operations are tied to long-cycle capital expenditure that is shielded from short-term macroeconomic volatility.

Valuation and Price Targets

Market participants have been slow to re-rate GEV since its separation from the parent company. Analysts who have closely followed the transition have begun to model a significant upside for the stock, with bullish price targets reaching as high as $1,150. This valuation suggests that the market is currently ignoring the quality of the company’s earnings growth and the durability of its order book.

For traders, the disconnect between GEV’s current trading range and its intrinsic value potential provides a rare opportunity. The company is not just selling hardware; it is selling the infrastructure backbone of the modern digital economy. As backlog conversion accelerates, investors should expect to see consistent margin expansion, which acts as a primary catalyst for a valuation re-rating.

What to Watch Next

Going forward, investors should keep a close eye on GEV’s quarterly order intake and the conversion velocity of its $150 billion backlog. Any signaling regarding further expansion in service-margin growth will be a key indicator that the company is successfully executing its transition toward a higher-quality earnings profile. Furthermore, monitoring policy shifts in grid modernization funding globally will provide a barometer for the durability of the current supercycle.

As the power demand narrative intensifies, GEV is transitioning from a 'wait-and-see' spin-off to a cornerstone industrial holding. The market may be underestimating what GE Vernova has already become, but the data suggests that the valuation gap is unlikely to persist as the company continues to deliver on its massive contractual commitments.