Back to Markets

Macro● Neutral

ECB Rate Hikes Loom as Nagel Demands Inflation Progress

Bundesbank President Joachim Nagel warns that the ECB will hike rates in June unless inflation projections improve, signaling a firm stance on price stability.

Continue with

Bundesbank President Joachim Nagel has signaled that the European Central Bank is prepared to resume its tightening cycle in June, contingent on the absence of a marked improvement in consumer price projections. This stance serves as a direct rebuttal to any interpretation that the Governing Council’s decision to hold rates steady last week represented a shift toward dovish hesitation. Instead, the pause is framed as a tactical delay intended to assess the geopolitical fallout from the conflict in the Middle East.

The Transmission of Geopolitical Risk to Policy

The ECB’s current policy framework relies heavily on the upcoming June 10-11 meeting, where new economic projections will serve as the primary catalyst for rate decisions. Nagel’s insistence on a hike in the absence of inflation cooling highlights a central bank prioritizing medium-term price stability over immediate growth concerns. The mechanism here is clear: if the energy-driven price shock continues to feed into broader inflation expectations, the ECB intends to use interest rates to anchor those expectations, even at the cost of suppressing economic activity.

This hawkish posture is not an isolated view within the Governing Council. Slovak central bank governor Peter Kazimir has described a June rate increase as all but inevitable. However, the internal consensus remains fragile. Greece’s Yannis Stournaras has publicly flagged the risk of a recession as a legitimate threat, suggesting that the transmission of policy tightening could hit a cooling economy harder than anticipated. This tension between inflation control and recession risk is the primary friction point for European markets.

Inflation Expectations and the Wage-Price Spiral

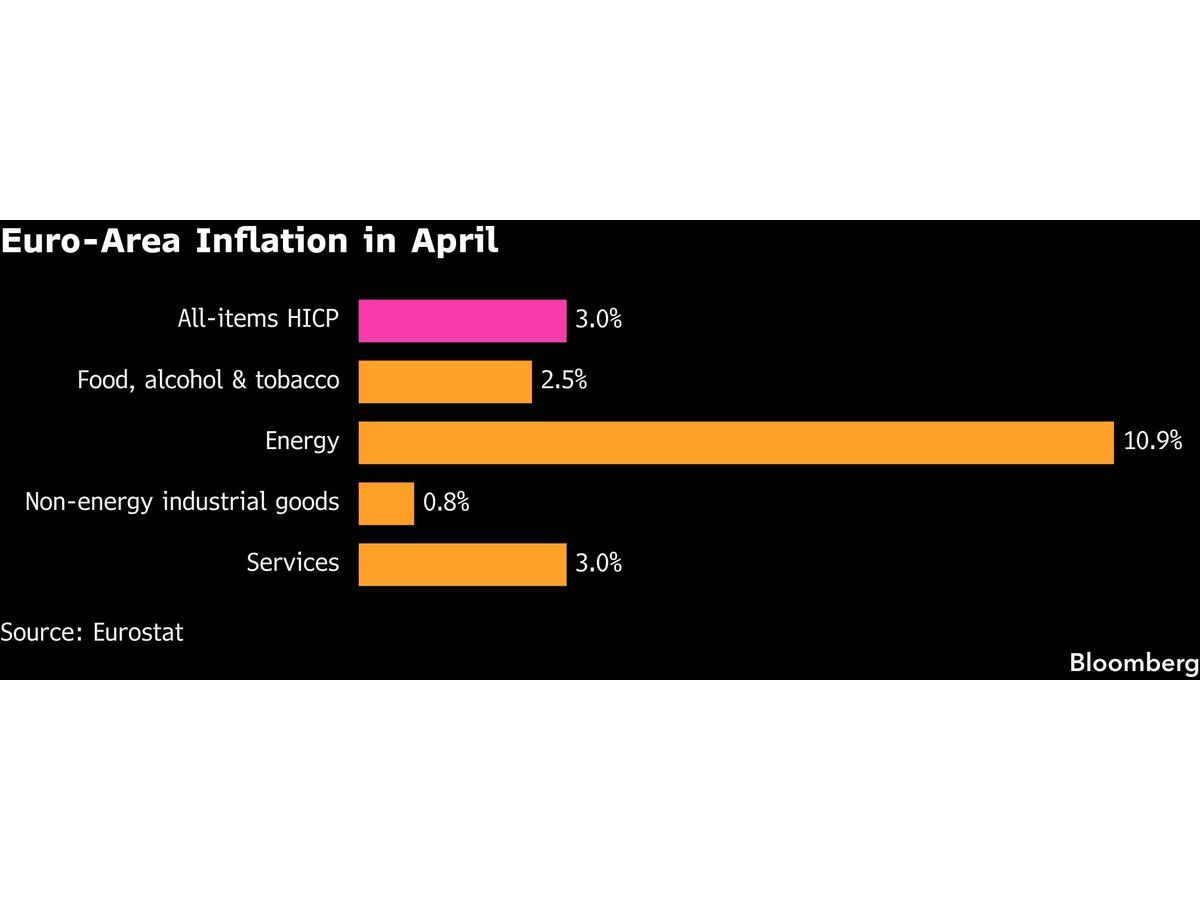

Nagel’s focus on the rise in medium-term consumer inflation expectations—which climbed to 3% in March from 2.5%—underscores the ECB’s fear of second-round effects. When expectations drift upward, the risk of a wage-price spiral increases, making the central bank’s job of returning inflation to its target significantly more complex. By signaling a readiness to act, Nagel is attempting to prevent these expectations from becoming entrenched.