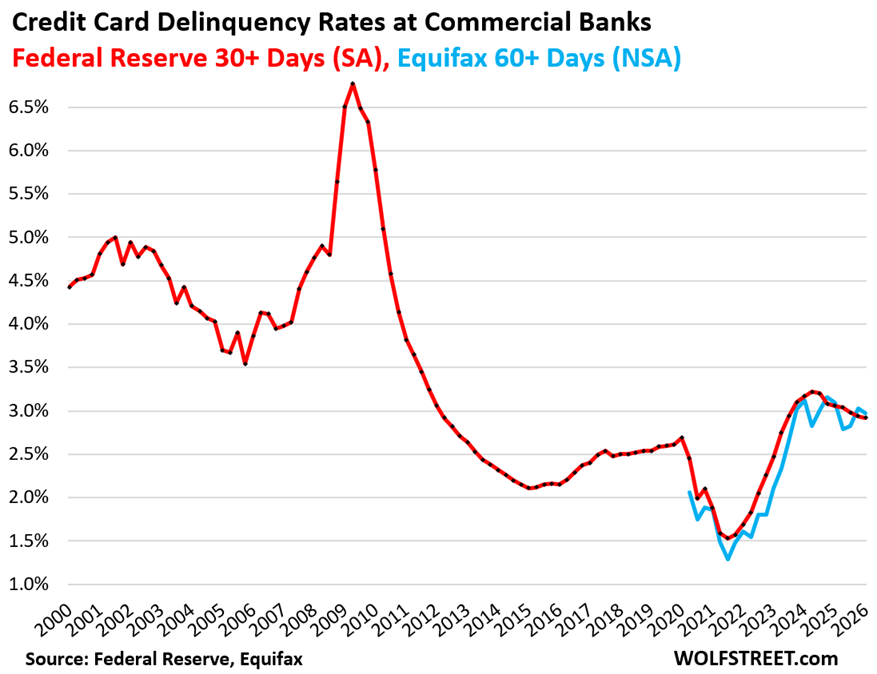

The 30-plus day delinquency rate on credit cards issued by all commercial banks fell to 2.92% in Q1 2026, seasonally adjusted. That is the lowest reading since Q2 2023, according to the Federal Reserve. The rate declined from 3.06% a year ago and 3.17% two years ago. The 60-plus day delinquency rate across all cards, including private label and subprime, dropped to 2.97% (not seasonally adjusted) from 3.09% a year ago, per Equifax.

For prime-rated cardholders, the 60-plus day delinquency rate measured by Fitch Ratings dipped to 0.94% – below pre-pandemic lows. The data confirms that the free-money hangover from 2020–2021 has largely dissipated. Consumer credit quality is improving, even as spending growth continues.

Why the Free-Money Hangover Has Worked Off

The Simple Read vs. The Better Market Read

The simple read: delinquency rates are falling, so consumer credit risk is benign. The better market read looks at the mechanism. The pandemic-era delinquency trough was artificially low because of government transfers and curtailed spending. When free money ended, delinquency rates rose out of that trough and overshot moderately. The overshoot was a normalisation, not a crisis. The subsequent decline over the past two years reflects a labour market that has not broken.

Key insight: The improvement is a lagging indicator of strong employment. As long as job gains hold above 150,000 per month, the income-to-spending feedback loop keeps delinquency contained.

Prime vs. Subprime: A Narrowing Gap

Prime cardholder delinquency at 0.94% is now lower than the pre-pandemic low point. During the pandemic-era peak, prime delinquency reached 1.07% – still below the 2017–2019 range. The subprime component, while not separately reported, is captured in the aggregate 60-plus day reading of 2.97%. That figure has declined from 3.12% two years ago. If subprime were deteriorating, the aggregate would rise. It is not. The delta is small but directionally consistent.

Balances Dip Seasonally, Spending Still Solid

Credit Card and Other Revolving Debt

Credit card balances – statement balances before payments – dipped by $28 billion (-2.2%) in Q1 from Q4 to $1.25 trillion, in line with the post-holiday seasonal pattern. Year-over-year, balances rose 5.9% ( $70 billion), driven by consumer spending and price increases. The New York Fed data based on Equifax confirms solid growth, not a spending binge.

“Other” consumer loans, including Buy-Now-Pay-Later (BNPL), personal loans, and payday loans, were roughly unchanged in Q1 and rose 3.7% year-over-year to $562 billion. That category has barely risen in 23 years despite population growth, income growth, and 83% CPI inflation – a point worth noting for anyone expecting a surge in unsecured consumer debt.

Debt-to-Income Ratio Remains Low

The ratio of revolving credit balances to disposable income dipped to 7.72% in Q1, below pre-pandemic Good Times levels. During the pandemic, the ratio plunged as spending on travel and dining collapsed while disposable income surged on government transfers. The ratio emerged from that trough in 2022 but has stayed below the 2017–2019 range. In a 23-year context, this is very low. Before the Financial Crisis, the ratio was much higher and caused havoc during the unemployment crisis that followed. That is not the case now.

Record Credit Limits and $4.23 Trillion in Unused Capacity

Banks have aggressively pushed credit card accounts, offering sign-up bonuses, cash-back rewards, and annual-fee premium cards. They also increased limits on existing cards to drive swipe-fee revenue. The aggregate credit limit rose by $60 billion in Q1 from Q4 to a record $5.5 trillion. Over the same period, balances dipped by $28 billion.

The available unused credit hit a record $4.23 trillion. Claims that Americans are “maxed out on their credit cards” do not match this data. The capacity to borrow is at an all-time high, and utilisation is low.

Collections at Rock Bottom: No Sign of Stress

Third-party collection entries are made when a lender sells delinquent debt to a collection agency. The New York Fed, via Equifax, reports that the percentage of consumers with collection entries has been creeping in the 5% range for over three years. That is down from 14% after the Great Recession. Large-scale job losses eventually lead to waves of debt sent to collections. With unemployment low, collections remain negligible. Any upward move from this floor would be noisy; the 30-day delinquency rate is the more reliable leading signal.

What Would Break the Trend

The Job Market as the Single Governor

The delinquency data is a lagging reflection of employment. A recession that pushes unemployment above 5% would reverse the trend. The current data shows no early warning signs of that. The Federal Reserve’s senior loan officer survey (due early May) is a leading indicator: tighter credit card standards would signal future stress.

Risk to watch: If the senior loan officer survey shows tighter standards, it would imply banks see rising risk in the unsecured consumer space. That would pre-date any delinquency spike by two to three quarters.

Affected Assets and Next Catalysts

- Credit card ABS: Prime ABS spreads have tightened. The improving delinquency data supports that. Stock market analysis shows risk premia in consumer ABS have compressed.

- Bank stocks: Major issuers benefit from lower charge-offs. Watch Q2 provisioning commentary from JPMorgan, Citigroup, and Capital One.

- Consumer discretionary: If delinquency remains low, consumer spending capacity stays higher. The shift from goods to experiences means the link is indirect.

| Metric | Q1 2026 | Prior Year | Change |

|---|

| 30+ day delinquency (SA, all banks) | 2.92% | 3.06% (Q1 2025) | -0.14pp |

| 60+ day delinquency (NSA, all cards) | 2.97% | 3.09% (Q1 2025) | -0.12pp |

| Prime 60+ day delinquency (Fitch) | 0.94% | ~1.00% est. | -0.06pp |

| Revolving credit balance | $1.81T | $1.72T (Q1 2025) | +5.2% YoY |

| Revolving debt-to-disposable income | 7.72% | ~8.0% est. | -0.28pp |

| Aggregate credit limit | $5.5T | $5.2T (Q1 2025) | +5.8% |

| Unused credit | $4.23T | $3.96T (Q1 2025) | +6.8% |

Practical rule: Improving delinquency data is a lagging indicator of a strong labour market. The risk of a sudden spike in credit card losses is low unless unemployment jumps. For now, the data supports a watch-list upgrade for consumer credit risk.

The next concrete data point is the Q2 2026 New York Fed Household Debt and Credit report (expected mid-August). If the summer spending season does not push delinquencies higher, the benign trend is confirmed. The collections data at 5% is so low that any upward move will be noisy – focus on the 30-day delinquency rate as the primary signal.