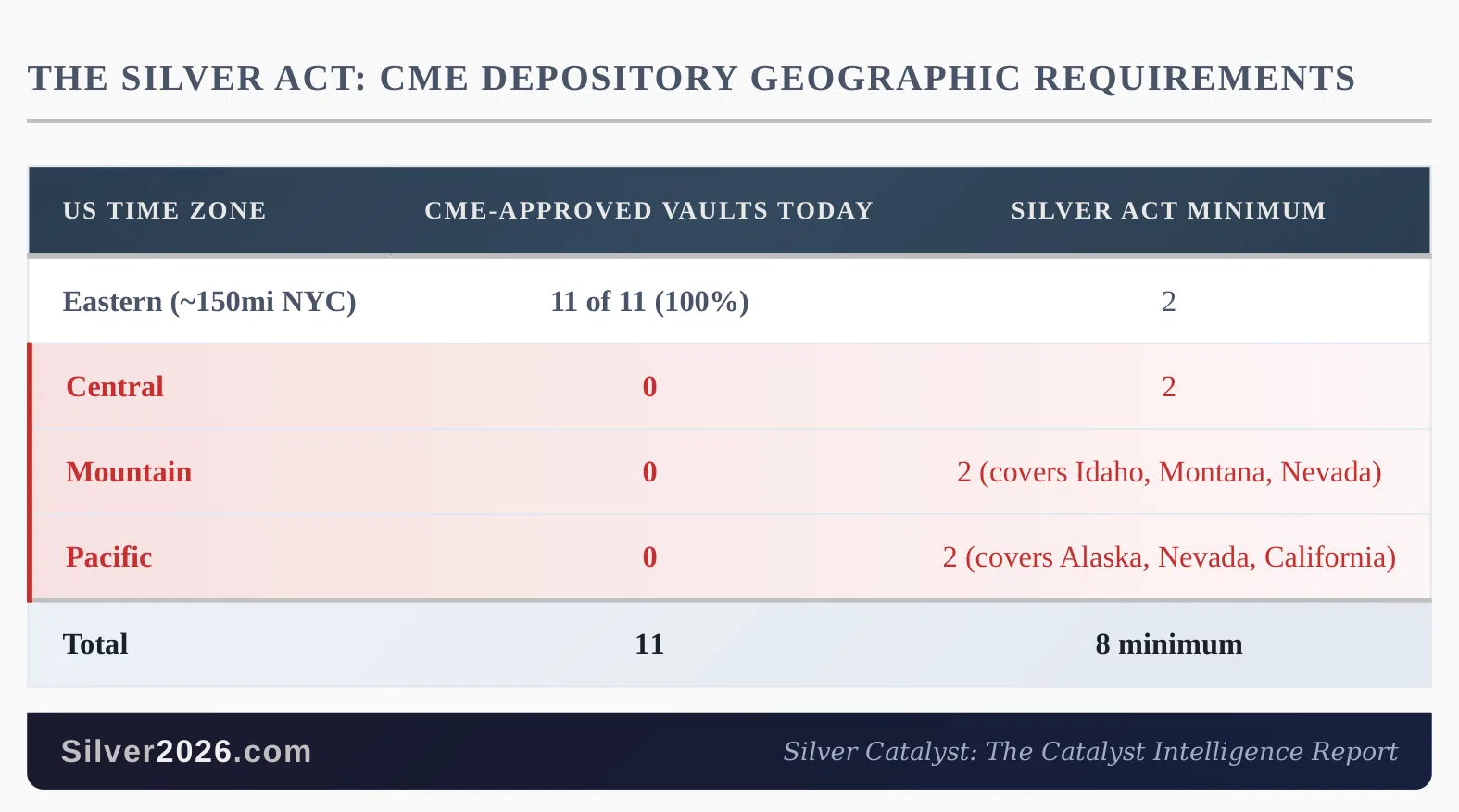

The regulatory landscape for precious metals shifted on April 16, when the Chairman of the US Commodity Futures Trading Commission (CFTC) publicly endorsed the System Integrity through Licensed Vault Expansion and Resilience Act (H.R. 8007). This legislative move, introduced by Rep. Russ Fulcher and Rep. Mark Harris on March 19, 2026, aims to mandate that derivatives clearing organizations select at least two approved depositories per US time zone for precious metals futures delivery. Currently, all 11 CME-approved silver depositories are clustered within 150 miles of New York City. This geographic concentration has long been criticized as a single-point-of-failure design that exacerbates price dislocations during periods of high demand or logistical stress.

The Mechanism of Market Concentration

The current structure forces physical metal to travel repeatedly between New York and London to satisfy COMEX delivery requirements, tariff-related shifts, and ETP redemptions. This reliance on a single geographic hub creates acute, temporary shortages when market conditions tighten. In January 2026, the system faced a significant stress test when 33.45 million ounces of silver were drawn from COMEX registered inventories in a single week. This volume represented approximately 25% of the total registered pool at that time, highlighting the fragility of a system lacking geographic diversity.

Further evidence of this structural limitation appeared in October 2025. According to the World Silver Survey 2026, ETP allocations absorbed such a large portion of London's available free float that "free silver" dropped to 17% of total inventories by the end of September. The resulting scarcity caused one-month lease rates to surge from 1% to over 30% in a matter of weeks. These episodes demonstrate that the market operates with fewer degrees of freedom than are required to absorb systemic shocks without significant price volatility. By decentralizing vaulting to the Mountain and Pacific time zones, where a substantial portion of US silver production occurs, the SILVER Act seeks to reduce transport bottlenecks and mitigate the risk of these acute, artificial supply squeezes.

Regulatory Stance and Legislative Outlook

While H.R. 8007 remains in committee with no scheduled markup, the CFTC Chairman's endorsement carries weight beyond the bill's immediate legislative prospects. The CFTC already possesses discretionary authority over depository approval criteria. By formally aligning with the decentralization argument, the regulator has signaled that the current concentration is a recognized national security risk and a contributor to price distortion. This public acknowledgment effectively changes the regulatory backdrop for the CME stock page, as the agency has now gone on record regarding the structural flaws of the current delivery mechanism. For traders, this means the regulatory pressure to diversify vaulting is unlikely to dissipate, regardless of whether the bill reaches a floor vote.

Impact on Paper-Physical Price Discovery

Silver is currently trading around $73, approximately 40% below its January 29 all-time high of $121.67 and 11% below the April 17 intraday peak. The persistent disconnect between the paper price and the fundamental deficit cycle has been a primary concern for market observers. If the SILVER Act is enacted, the second-order effect would be a more responsive price discovery mechanism. Geographic dispersion of vaulting makes it structurally more difficult to sustain the paper-physical disconnect that has characterized recent years. When the market operates with more degrees of freedom, the effectiveness of artificial price suppression or lease rate manipulation is theoretically reduced.

Current Market Positioning and Risks

Investors should note that the current consolidation in silver is driven by a confluence of factors: persistent dollar strength, the fading of ceasefire optimism, and the ongoing transition at the Federal Reserve. The Senate Banking Committee voted 13-11 on April 29 to advance the nomination of Kevin Warsh, with a full Senate vote expected the week of May 11, coinciding with the end of Jerome Powell's term. Furthermore, the COMEX May delivery cycle presents its own set of risks, with 153 million ounces in paper open interest against 77.12 million ounces of registered metal, with First Notice Day occurring on April 30.

Despite these short-term pressures, the long-term fundamental picture remains defined by a six-year deficit cycle and flat mine production, even after a 42% annual average price increase in 2025. With COMEX registered inventory covering only 13.4% of total open interest, the market remains susceptible to volatility. The CFTC's recent testimony provides a new framework for understanding these dislocations, suggesting that the structural issues in the silver market are no longer being ignored by the regulators tasked with their oversight. Traders should monitor future committee hearings for any indication that the CFTC intends to exercise its existing discretionary authority to force vaulting decentralization even in the absence of new legislation.