Christian Freytag, Allianz's chief technology officer, said June 3 at Insurtech Insights in New York that artificial intelligence now represents a greater risk to insurers than business interruption or natural catastrophes. He pointed to quantum computing-enhanced cyberattacks as a priority threat requiring intensified focus within two to three years.

The NAIC's Model Bulletin on AI systems affirms that existing unfair discrimination laws apply regardless of the technology used. Colorado, New York, and California have each issued additional guidance on algorithmic underwriting. Carriers relying on third-party scores or AI-assembled property files must be able to explain what data drove a premium increase, repair demand, or nonrenewal. Policyholders must have a documented path to correct inaccurate information. Black-box processes invite enforcement exposure.

Executives from Allianz, New York Life, TIAA, and Tokio Marine outlined a measured approach at the same event. New York Life CIO Deepa Soni projected 'substantial' operational impact from AI within five years, emphasizing friction reduction in advisor workflows. Tokio Marine's Robert Pick cautioned against moving faster than governance frameworks can support. The consensus, panelists said, is that AI must remain a tool rather than a decision-maker.

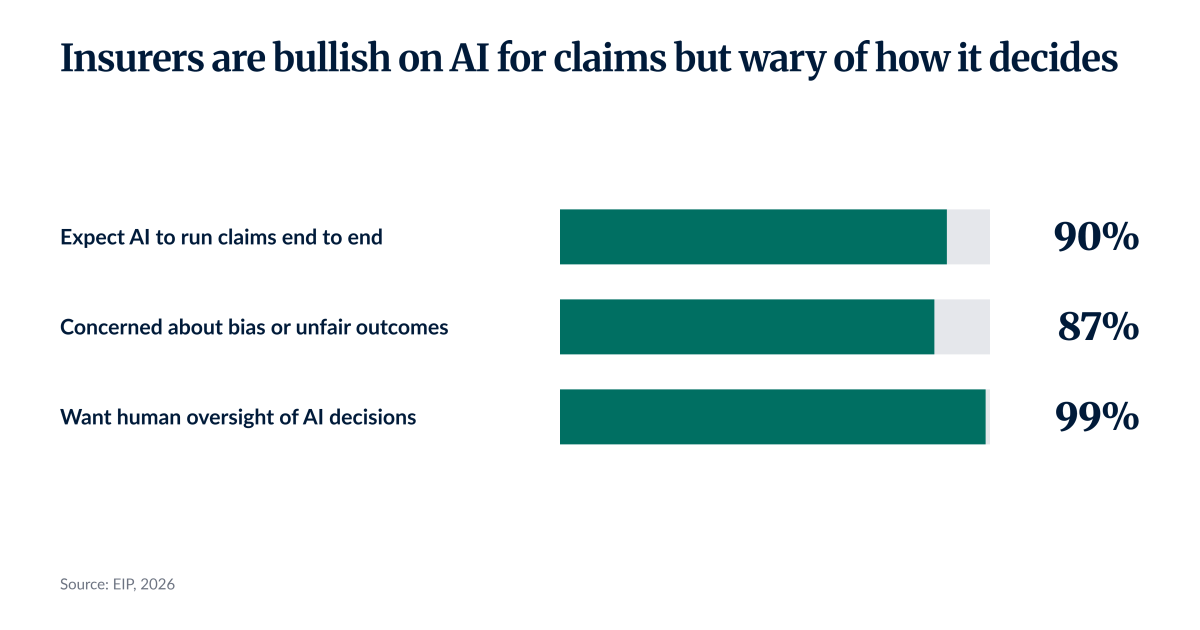

Claims automation brings a similar regulatory burden. Branch Insurance now processes 85% of first notice of loss contacts through digital or voice AI channels. Full automation of claims decisions exposes carriers to regulatory scrutiny and reputational risk. Liberate's AI platform can handle 6,000 calls per second, critical during catastrophe events when human agents are overwhelmed. AI voice tools detect tone and urgency to route calls appropriately and feed live agents real-time information, lifting call-quality scores across experience levels.

Commercial auto fleets are another line where AI shifts the risk profile. Rising claim frequency, severity, and nuclear verdicts make fleets prime targets for plaintiffs' attorneys. API-connected ELDs, dashcams, and telematics give carriers objective data for litigation-versus-settlement decisions. AI platforms can push underwriting throughput beyond the five to 10 accounts a day a skilled underwriter can manually process. Fleet operators can reduce exposure by tightening driver hiring standards and evaluating insurers on loss ratios rather than price.

Specialty lines carry their own hazards. Automating underwriting in cyber and errors-and-omissions coverage risks missing subtle policy characteristics, executives warned. Any model failure in those lines shifts concern immediately from efficiency to claims exposure.

The push into AI also creates vendor risk. Many insurtech firms operate at a loss while overpromising, executives said. Financial viability is as critical an evaluation criterion as technical capability. Carriers and MGAs are standing up AI committees with formal decision ownership, audit trails, and explainability requirements. Water damage costs U.S. insurers nearly $13 billion annually, with claims averaging more than $15,000. Carriers moving toward continuous risk assessment verify that smart home mitigation systems remain operational throughout the policy term.

Berkshire Hathaway's insurance operations, including Geico, write large volumes of auto and property policies. The regulatory and litigation pressures described above apply to any carrier using AI for decisions. AlphaScala's proprietary model gives BRK.B a score of 49 out of 100, labeled 'Mixed', reflecting the combined pressures and possibilities.

Oklahoma's party primaries are set for June 18. The winner will have roughly seven months to act on some of the nation's highest premium rates and decide how to regulate AI in insurance. Republican candidate Bob Sullivan has called for mandatory disclosure when algorithms influence underwriting, pricing, or claims.