The euro-denominated stablecoin consortium Qivalis has secured backing from 37 banks across 15 European countries and plans to launch in the second half of 2025. That number of institutional signatories at inception is unusual in digital-asset infrastructure. Most euro stablecoins today come from non-bank issuers: Circle’s EURC and Binance’s BUSD-E. Qivalis’s bank-led model changes the counterparty profile and, potentially, the liquidity argument.

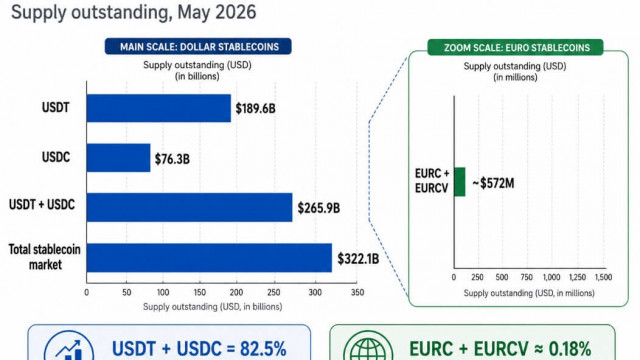

The read-through is not about another euro-pegged token. It is about whether a regulated bank consortium can shift the dominant settlement currency in decentralised finance from the dollar to the euro. The stablecoin market runs on USDT and USDC, which together account for roughly 90% of on-chain volume. Euro-denominated equivalents hold a single-digit share. Qivalis’s launch structure – 37 banks willing to issue and distribute the token – could narrow that gap if the consortium achieves scale.

Why Bank-Backed Euros Change the Stablecoin Calculus

Existing euro stablecoins struggle with liquidity fragmentation and limited exchange listings. The naive interpretation is that more bank logos solve those problems. The better market read is different. Bank backing does not automatically create liquidity. It does alter the redemption path. A token redeemable directly at 37 member banks, governed under EU licensing, reduces the settlement risk that sometimes keeps large euro-block market makers on the sidelines. That mechanism could drive adoption, not branding.

The liquidity challenge remains. Even a well-capitalised euro stablecoin needs depth on centralised exchanges and DeFi pools to compete with USDT and USDC. Those two tokens have years of network effects. Qivalis will need to seed pools, secure listings, and attract the market makers that currently route most flow through dollar pairs. The consortium structure may help with distribution on the banking side – corporate treasuries, payment rails – but on-chain liquidity is a separate problem.

What This Means for Dollar-Denominated On-Chain Finance

For traders building watchlists, the Qivalis launch tests a structural question: if a credible euro stablecoin reaches meaningful circulation, does DeFi activity start to denominate in euros rather than dollars? The short answer is not yet. The longer answer depends on interest-rate differentials, regulatory clarity, and the willingness of centralised exchange operators to quote euro-stablecoin pairs as base pairs. No exchange today lists EUR as a primary quote currency for major crypto pairs. That would have to change for Qivalis to matter beyond niche use.

The consortium’s timeline – second half of 2025 – coincides with the expected implementation of MiCA stablecoin rules across EU member states. That regulatory framework gives euro stablecoins a compliance advantage over dollar tokens that are not always MiCA-compliant. The question is whether issuers like Circle will adapt their products or cede the euro corridor to bank-led projects.

Qivalis as a Tokenisation Sector Signal

The 37-bank consortium is also a supply-chain event for the tokenisation sector. If banks issue their own stablecoin, they are more likely to build on-chain settlement rails for other tokenised assets – bonds, funds, real estate. That premise drove JPM Coin and the Monetary Authority of Singapore’s Project Guardian. Qivalis extends the model to a multi-jurisdiction euro zone, which adds complexity but also network coverage. For earlier moves in tokenisation, see our article on REAL Finance Signs $100M Tokenization Pact with Factori AD.

The counterparty risk of a bank-backed stablecoin is low relative to unbacked or single-issuer tokens. Execution risk is high: coordinating 37 banks across 15 countries on a single token standard, custody model, and compliance playbook is a heavy operational lift. If Qivalis delays or scales down, the read-through for other bank-led stablecoin projects will be negative. If it launches on time and achieves meaningful market capitalisation within its first year, competitive pressure on dollar stablecoins becomes real.

The next marker is the regulatory filing under MiCA, which will disclose the reserve composition, custody arrangements, and licensed entities. That filing will clarify whether Qivalis is a true single token or a network of interoperable bank-specific tokens under one brand. For now, the 37-bank consortium signals that Europe’s banking sector wants a native on-chain euro. Whether it gets one that draws liquidity away from the dollar depends on execution details that will emerge over the next two quarters.