Stocks● Neutral

Why 32% of Insurance M&A Deals Destroy Corporate Value

Analysis of 500 carrier transactions reveals that most mergers fail to move the needle. Expect a cooling in deal volume as shareholders demand better returns.

Continue with

The Hidden Cost of Consolidation

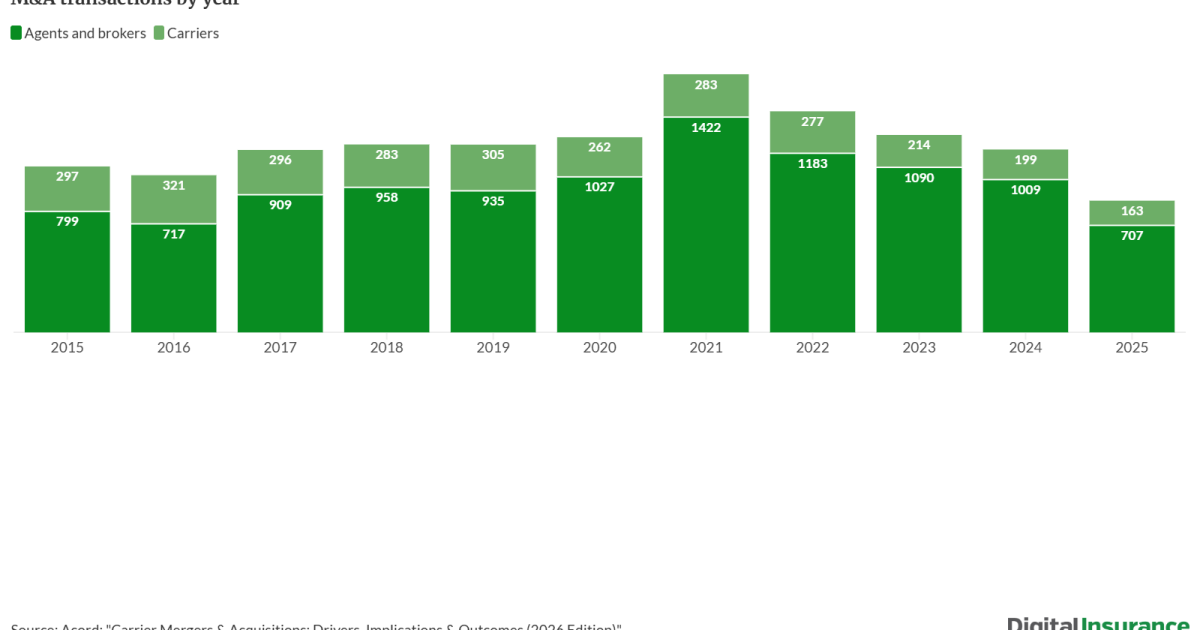

Insurance companies are finding that growth through acquisition is a double-edged sword. A new study from Acord reveals that 32% of insurance M&A deals actively destroy organizational value rather than create it. The research, which analyzed 500 carrier transactions conducted in 2026, highlights a disconnect between deal intent and post-merger reality.

Executives often pursue acquisitions to capture market share or expand their market analysis capabilities. However, the data confirms that these ambitions frequently fail to translate into shareholder returns. When companies prioritize scale over operational integration, the consequences show up directly on the balance sheet.

Analyzing the Failure Rates

The Acord report categorizes the outcomes of these 500 transactions based on long-term performance metrics. The distribution of value creation reveals a sobering reality for boards of directors:

- 32% of deals: Destroyed organizational value.

- 40% of deals: Remained value-neutral.

- 28% of deals: Provided genuine value creation.

These figures suggest that most insurance mergers fail to move the needle for investors. While firms often justify high premiums by citing synergies, the actual execution of these integrations remains a primary point of failure. If you are tracking momentum investing, these failure rates suggest that growth-by-acquisition strategies require deeper skepticism.