Back to Markets

Macro● Neutral

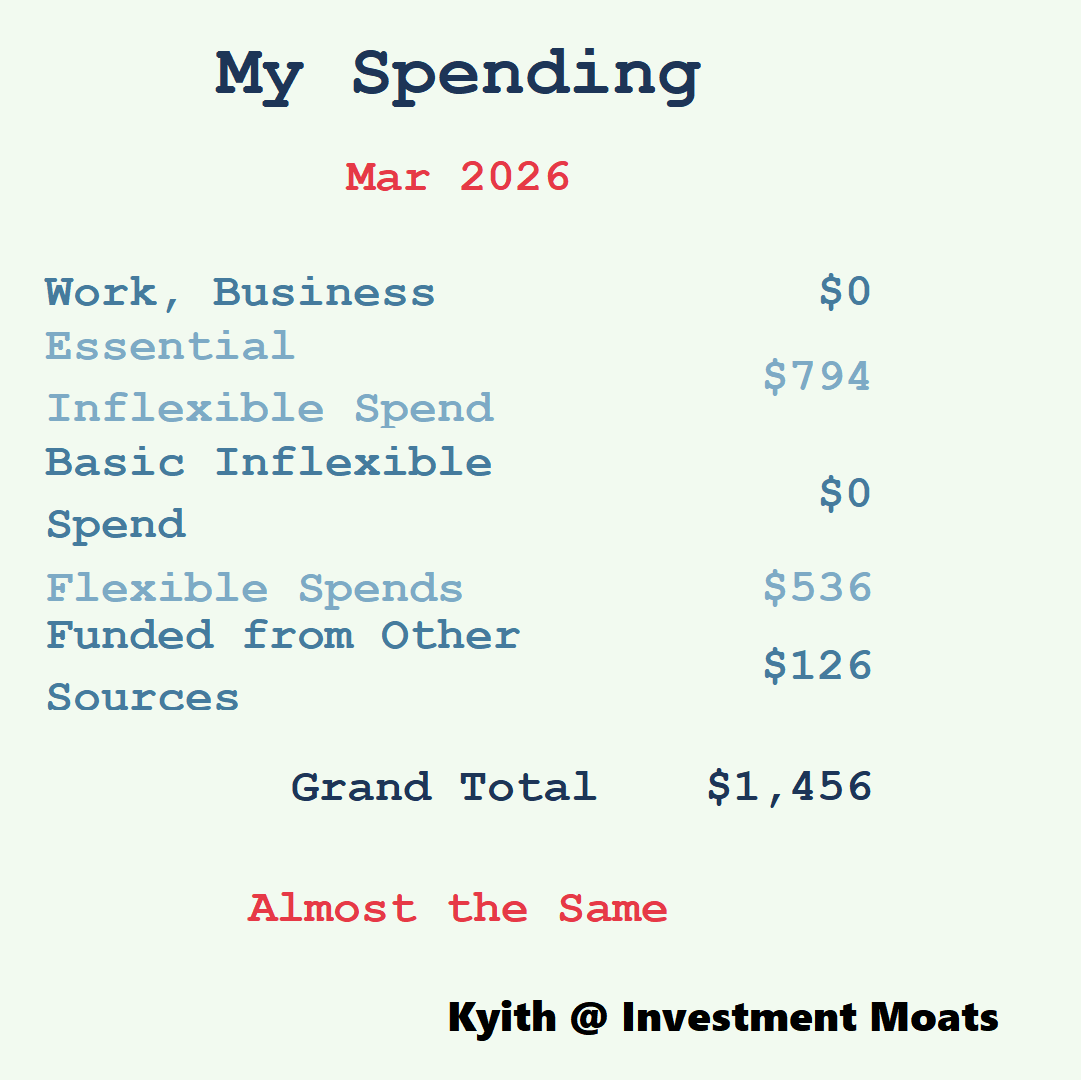

Why Tracking Your $1,456 Monthly Burn Rate Protects Portfolios

Auditing personal cash flow acts as a diagnostic tool against market volatility. Master your $1,456 expenditure benchmark to prevent panic-selling in 2026.

Continue with

The Discipline of Micro-Accounting

In the realm of personal finance and wealth accumulation, the most significant variable often lies not in the high-level volatility of the S&P 500 or the fluctuations of the bond market, but in the granular management of individual cash flow. For March 2026, personal expenditure was recorded at exactly $1,456. While this figure serves as a singular data point, it represents a critical exercise in financial accountability—a practice that professional traders and retail investors alike often neglect to their own detriment.

Tracking expenses is not merely an administrative chore; it is a fundamental diagnostic tool. By auditing every dollar allocated to lifestyle maintenance, an investor can determine their 'burn rate,' which directly informs the size of the emergency fund required to withstand market drawdowns or periods of professional transition. For the disciplined investor, $1,456 serves as a benchmark for lifestyle inflation, providing a baseline to measure against future periods of volatility.

Contextualizing the $1,456 Benchmark

To understand the significance of this figure, one must look at the broader context of personal financial management. Maintaining a lean expenditure profile—such as the $1,456 recorded in March—is the primary engine for capital allocation. In an era of persistent inflationary pressure, the ability to control one's cost of living is analogous to a firm optimizing its operating expenses (OPEX) to preserve net margins.

Historical data suggests that those who maintain detailed spending logs are better positioned to capitalize on market opportunities. By treating personal finance with the same rigor as corporate accounting, individuals can identify 'leaks' in their budget that would otherwise be funneled into depreciating assets rather than compound-interest-bearing vehicles. The methodology used to arrive at this $1,456 figure involves a structured grouping of outflows, allowing for a clear distinction between essential sustenance and discretionary spending.