Strong Start for Asset Management Giant

BlackRock reported a strong opening to the year, beating Wall Street expectations for the first quarter of 2026. The world's largest asset manager saw its earnings bolstered by a surge in demand for its technology services and subscription offerings, signaling a shift in how the firm generates value beyond traditional management fees.

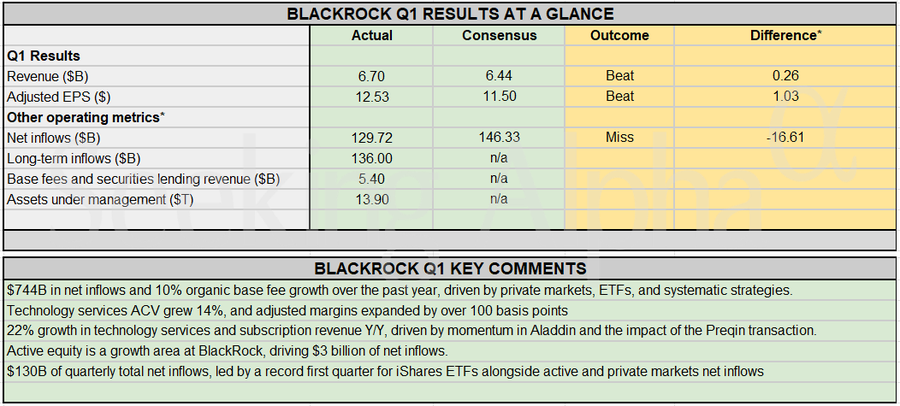

Total revenue for the quarter reached $5.7 billion, topping analyst estimates. The firm's focus on diversifying its income streams is paying off, as clients increasingly rely on BlackRock's proprietary software platforms to manage their own investment portfolios.

Tech Services Drive Growth

The standout performer in the latest report was the technology services division. Revenue from this segment climbed 22% year-over-year, proving that BlackRock is no longer just an asset manager but a critical provider of financial infrastructure.

Investors looking for deeper stock market analysis should note how these recurring subscription fees provide a buffer against the volatility typically found in asset-based revenue. The following table breaks down the growth drivers for the quarter:

| Metric | Growth (YoY) | Key Takeaway |

|---|

| Tech Services Revenue | 22% | Primary growth engine |

| Subscription Fees | 22% | High-margin, stable income |

| Total Revenue | $5.7B | Exceeded expectations |

Strategic Focus on Recurring Income

BlackRock's leadership emphasized that the shift toward subscription models is a core pillar of their business strategy. By locking in long-term contracts with institutional clients, the company is insulating its bottom line from market swings.

"Our technology and subscription businesses are delivering consistent, high-quality growth that differentiates us in the current environment," the firm noted in its earnings release.

This trend is keeping the firm ahead of competitors who remain tethered to traditional fee structures. Traders often compare these results to broader best stock brokers to gauge how financial service firms are adapting to the digital shift.

Market Implications and Outlook

For investors, the primary takeaway is the resilience of BlackRock's non-asset-based revenue. While market downturns can compress asset values and lower management fees, the technology division continues to scale regardless of daily market fluctuations.

Looking ahead, market participants should watch for:

- Expansion of Aladdin platform usage: Further integration with institutional clients will likely sustain double-digit growth in tech services.

- Asset flows: Monitor net inflows into ETFs and private credit products to see if they match the growth seen in the tech division.

- Operating margins: Continued investment in software development may fluctuate, but the recurring nature of subscriptions should support long-term profitability.

BlackRock’s ability to turn its internal software into a commercial product remains a key differentiator. If this momentum holds, the firm will continue to decouple its earnings potential from the performance of global equity markets.