The Geopolitical De-escalation Dividend

For several weeks, the global fixed-income market was held hostage by the specter of a broader Middle Eastern conflict. The resulting uncertainty sent investors sprinting toward the safety of sovereign debt, compressing yields as the market priced in a geopolitical risk premium. However, as a fragile ceasefire between the U.S. and Iran takes hold, the 'safe-haven' trade is rapidly unwinding. With the immediate threat of a supply-side energy shock receding from the headlines, bond traders are performing a sharp pivot, refocusing their scrutiny on the one variable that has consistently defied central bank efforts: persistent inflation.

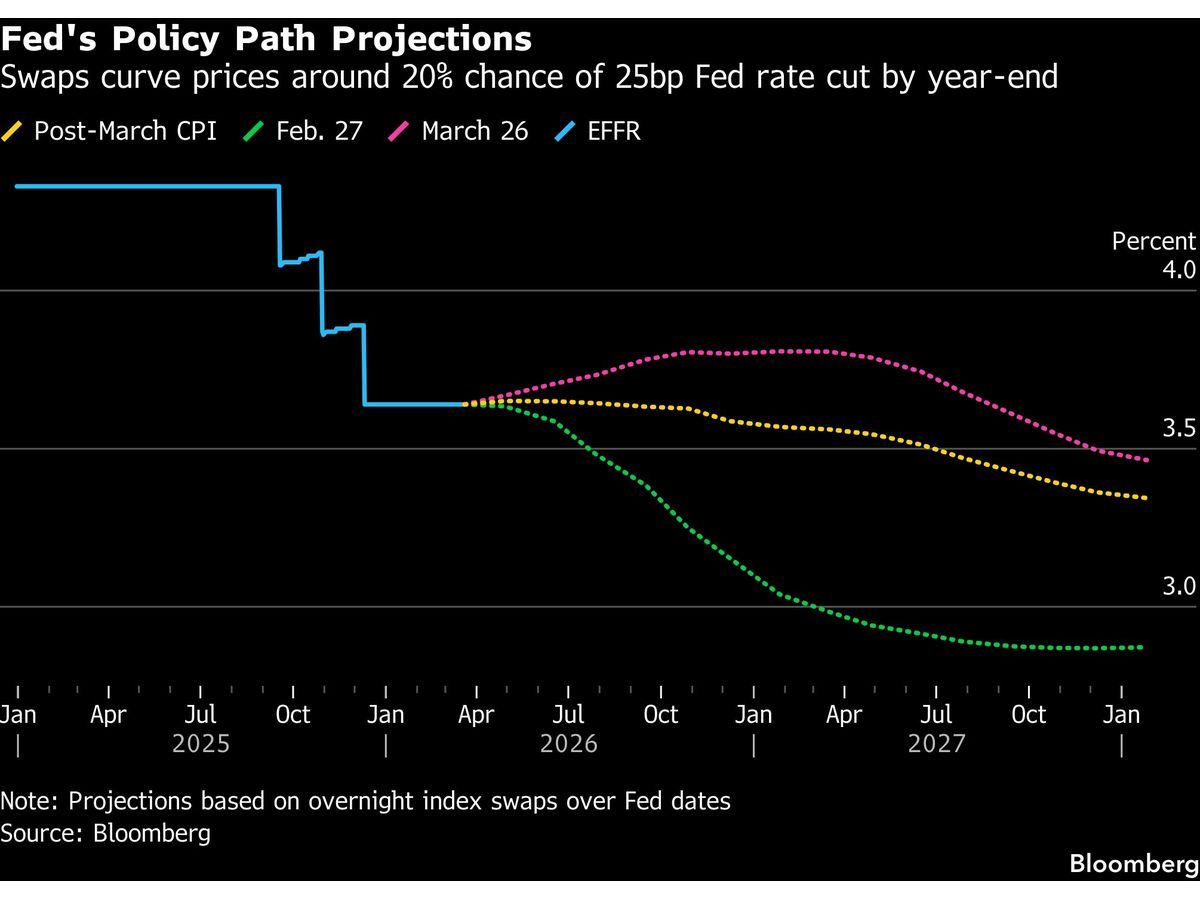

The Return of the 'Higher-for-Longer' Mandate

As the geopolitical distraction fades, the stark reality of macroeconomic fundamentals is reasserting itself. The bond market is recalibrating to the reality that the Federal Reserve remains in a 'higher-for-longer' interest rate environment. Despite previous market optimism surrounding potential rate cuts, the current data suggests that the path to the Fed’s 2% inflation target is far more arduous than previously modeled.

Traders are now aggressively repricing the yield curve, recognizing that a resilient labor market and sticky service-sector inflation provide the Federal Reserve with ample cover to maintain restrictive monetary policy. The recent sell-off in long-dated Treasurys reflects a growing consensus that capital costs will not retreat as quickly as the bulls had hoped. For institutional players, this means the 'duration trade'—which saw significant inflows during the height of the Iran-U.S. tensions—is being liquidated in favor of re-evaluating the terminal rate.

Market Implications: Navigating the Yield Rebound

For traders, the shift back to an inflation-centric narrative introduces significant volatility. As bond prices fall and yields climb, the cost of borrowing rises, which naturally puts pressure on equity valuations, particularly in the growth and technology sectors. When risk-free rates remain elevated, the discounted cash flow models used to value high-growth stocks become increasingly sensitive, often leading to multiple compression.

Furthermore, the correlation between oil prices and bond yields is tightening once again. While the ceasefire has provided a temporary reprieve for energy markets, any resurgence in regional instability would instantly resurrect the inflation-bond-yield feedback loop. Investors should monitor the spread between nominal yields and inflation-protected securities (TIPS) as a primary indicator of whether the market expects inflation to remain structurally embedded.

What to Watch: The Fed’s Next Move

Looking ahead, the focus shifts squarely to upcoming labor market reports and CPI prints. The market is currently in a 'wait-and-see' mode regarding the Federal Open Market Committee (FOMC) meeting minutes. If the economic data continues to show resilience, the market may be forced to push back the timing of the first rate cut even further into the calendar.

Traders should be prepared for a environment where 'good news is bad news.' In this current cycle, positive economic growth data—while beneficial for corporate earnings—only serves to strengthen the argument for the Fed to keep the pedal on the monetary brake. As we move through the next quarter, expect yield curve volatility to remain elevated as the market reconciles the disconnect between potential geopolitical calm and the underlying, stubborn inflationary pressures of the U.S. economy.